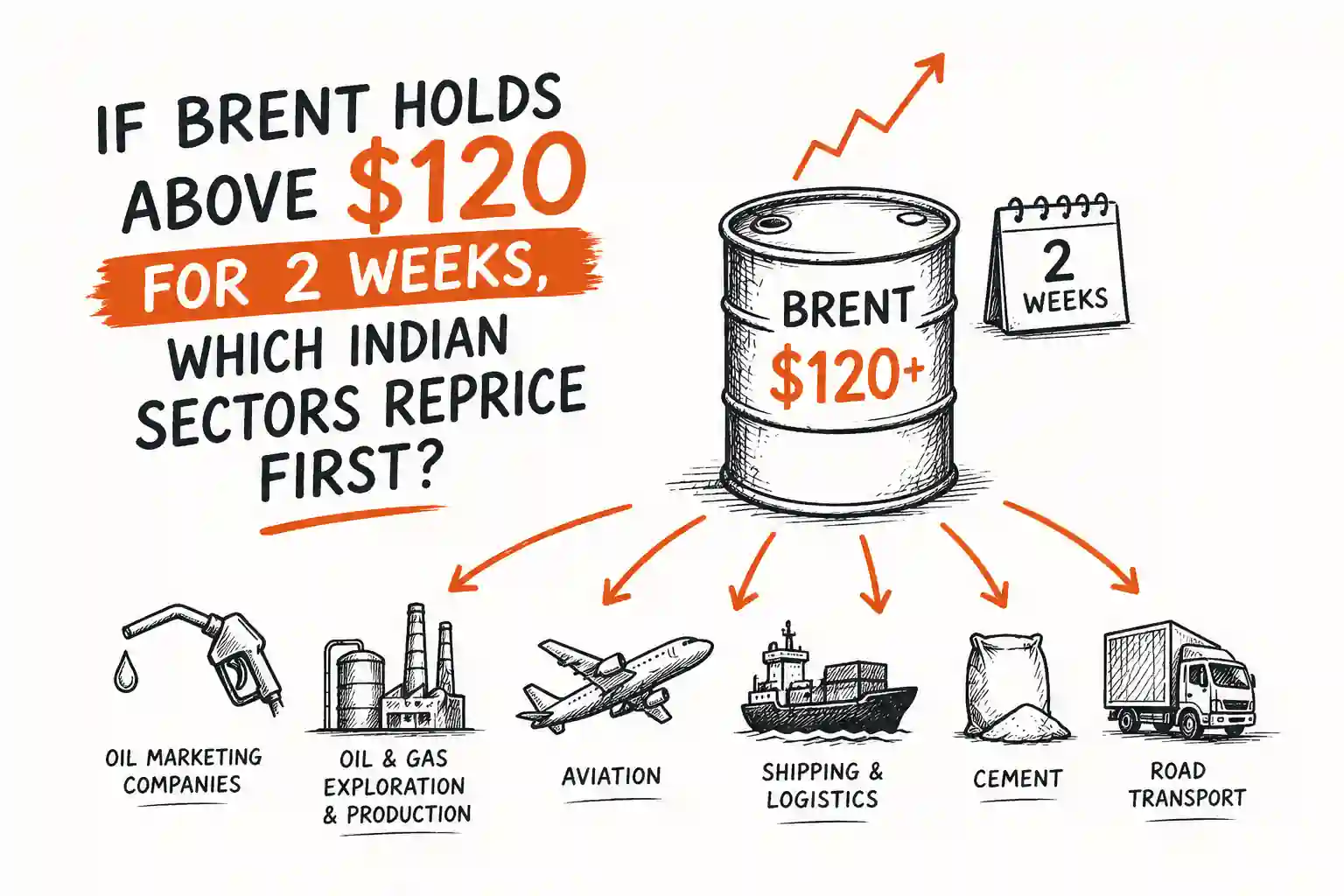

If Brent Holds Above $120 for 2 Weeks, Which Indian Sectors Reprice First?

If you want to understand the Brent above $120 impact on Indian sectors, the first thing to watch is not the price spike itself but the duration. A one-day move can be dismissed as panic. A two-week stretch above $120 is harder to wave away. At that point, markets begin to assume that the oil shock may feed into inflation, the rupee, bond yields, and earnings expectations. That is when repricing spreads beyond the obvious fuel-sensitive names.

| Sector | Direct oil | Rupee | Yields | Speed | Overall |

| Aviation | Very high | High | Medium | Very fast | Very high |

| Tyres | High | Medium | Medium | Fast | High |

| OMCs | Very high | Medium | Medium | Fast | High |

| Banks / NBFCs | Low | High | Very high | Medium | High |

| Metals | High | Medium | Low | Medium | Medium |

| Capital goods / infra | Medium | Medium | High | Slow | Medium |

| FMCG | Medium | Medium | Low | Slow | Low to medium |

| IT exporters | Low | Low to medium | Low | Slow | Low |

The first sectors to reprice are the direct crude losers

The earliest damage usually shows up in businesses where fuel and energy costs hit quickly. Aviation is the cleanest example. Airlines feel crude pain almost immediately because fuel is one of the biggest moving parts in the profit equation. If Brent stays elevated, the market starts cutting margin assumptions before companies even report it.

Tyre makers also come under pressure early. Their raw-material basket is not driven by crude alone, but energy-linked costs still matter enough for investors to reassess profitability when oil stays high. Oil marketing companies are another early battleground. Their problem is more complicated because crude exposure gets mixed with pricing policy, inventory effects, and margin uncertainty. That makes them vulnerable when traders stop treating the move as a temporary spike and start treating it as a tougher operating environment.

This is why crude-sensitive stocks often react first. The market does not need perfect earnings clarity here. It only needs enough evidence that the cost base is moving in the wrong direction.

The second wave usually hits banks and financials

This is where the oil story becomes more interesting. Banks do not buy crude, but they do trade inside the macro backdrop crude creates.

If Brent remains above $120, inflation pressure stays alive. A weaker rupee makes that pressure worse by raising imported costs further. Once that happens, the Reserve Bank of India has less room to sound accommodative, and bond yields tend to stay firm. That changes the valuation backdrop for banks and NBFCs.

This is why Bank Nifty weakness in an oil shock matters. It is often a sign that the market is moving from direct sector pain to a broader financial-conditions reset. Higher yields, tighter liquidity expectations, and a less friendly policy backdrop can all weigh on financials, even before loan growth or asset quality visibly deteriorate.

In practical terms, if private banks and rate-sensitive financial names start lagging alongside a weak rupee and firm yields, the market is no longer reacting only to fuel costs. It is repricing macro risk.

→

Import bill rises

→

Rupee weakens

→

Inflation risk rises

→

RBI flexibility narrows

→

Yields stay elevated

→

Banks and cyclicals reprice

Metals and cyclicals come under pressure next

The third layer is usually cyclical. Metals, capital-heavy businesses, and other economically sensitive sectors become more fragile once investors start worrying about both costs and demand.

Metals are a good example because the usual shortcut can be misleading. A weaker rupee can help exporters at the margin, but that benefit is limited if energy costs are rising and global demand expectations are turning softer. In that setup, margins can get squeezed from both sides.

Capital goods and infrastructure names can also become less resilient if elevated crude feeds into higher yields and a tighter funding environment. In a calm market, investors are willing to pay for long-duration growth stories. In a stressed market, they become less patient about delays, execution risk, and premium valuations.

That is when an oil shock stops being a narrow sector event and becomes a broader de-risking move across Indian equities.

What usually holds up better

Not every sector gets hit at the same speed. Businesses with stronger pricing power, lower direct energy intensity, and healthier balance sheets can hold up better at first. Some defensives may even look stable for a while.

But that does not automatically make them safe. If high crude persists long enough, the issue broadens from direct cost pressure to a more general repricing of inflation, yields, currency risk, and growth expectations. In other words, the market can move from rotation to outright derating.

What traders should watch if Brent stays above $120

If this oil shock persists, four signals matter more than the headlines.

First, the rupee. If it keeps weakening, imported inflation becomes harder to contain.

Second, Indian bond yields. If the 10-year yield stays above 7 percent or pushes higher, valuation pressure is likely to spread beyond the direct crude losers.

Third, Bank Nifty relative strength. If banks remain weak even during broader market rebounds, it usually means the shock is moving deeper into the financial system.

Fourth, sector breadth. If airlines, tyres, OMCs, logistics, and selected industrial names all keep weakening together, the repricing is becoming broader and more durable.

A signal-driven trading view of the oil shock

This is where an AI trading or systematic framework can actually be useful. The real advantage is not prediction. It is early classification.

A signal-driven oil-stress model would monitor a small set of variables together instead of looking at each one in isolation.

| Scenario | What it means | Sectors hit first | What to watch next |

| Sector-only stress | Crude-sensitive names weaken, but the rupee, banks, and yields stay relatively contained. | Aviation, tyres, OMCs | Whether banks and bond yields stay calm |

| Macro spillover | Oil stays high, the rupee stays weak, yields remain elevated, and financials begin to lag. | Banks, NBFCs, metals | Bank Nifty relative weakness and broader breadth damage |

| Full risk-off | Oil remains high, the rupee worsens, yields rise, and large-cap selling broadens. | Financials, cyclicals, large-cap index names | FII selling, VIX, breadth, and support levels |

That distinction matters because the market behaves very differently in each phase. A short-lived oil spike can often be faded. A persistent oil shock forces the market to reprice in sequence.

That is the real takeaway. If Brent holds above $120 for two weeks, Indian equities are unlikely to move as one block. Airlines and tyres may feel it first. Banks may feel it next. Metals and capital-heavy cyclicals may come under pressure once the market accepts that expensive crude is no longer a headline but a condition.

Not investment advice. Always do your own research before trading.

Share this insight

Spread the Alpha

Related Articles

More ideas that align with your trading playbook.

Reliance AGM 2026 Highlights: Jio IPO, AI and New Energy Plans Explained

Reliance Industries’ annual general meetings usually come with big announcements. The 2026 AGM was no different. But beneath the new products, ambitious…

SEBI’s Commodity Plan Just Lost Its Institutional Anchor. What It Means for MCX

SEBI wanted banks, insurers, and eventually pension funds to deepen India's commodity derivatives market. RBI and IRDAI are not inclined to allow…

India’s Data Center Power Trade: Which Stocks Benefit First if AI Infra Spending Accelerates?

India's AI buildout may look like a software story, but the first listed winners could emerge from transformers, cables, switchgear, backup power,…

DailyBulls (Arthashilpi Ventures) is a D-U-N-S verified company.

DailyBulls (Arthashilpi Ventures) is a D-U-N-S verified company.