India Capital Goods: How to Judge Order Book Quality (2026)

Quick take

- Order-book size is just a starting signal.

- Better stock outcomes usually come from three things: conversion quality, margin quality, and cash-flow quality.

- If order inflow goes up but receivable days also go up, quality risk is rising.

- Book-to-bill looks good on paper, but without execution discipline it can mislead.

- In this cycle, the biggest mistake is paying expensive valuations for weak cash-conversion businesses.

This is the first deep-dive after our Make in India 2.0 capex playbook, focused on the quality of capital goods order books.

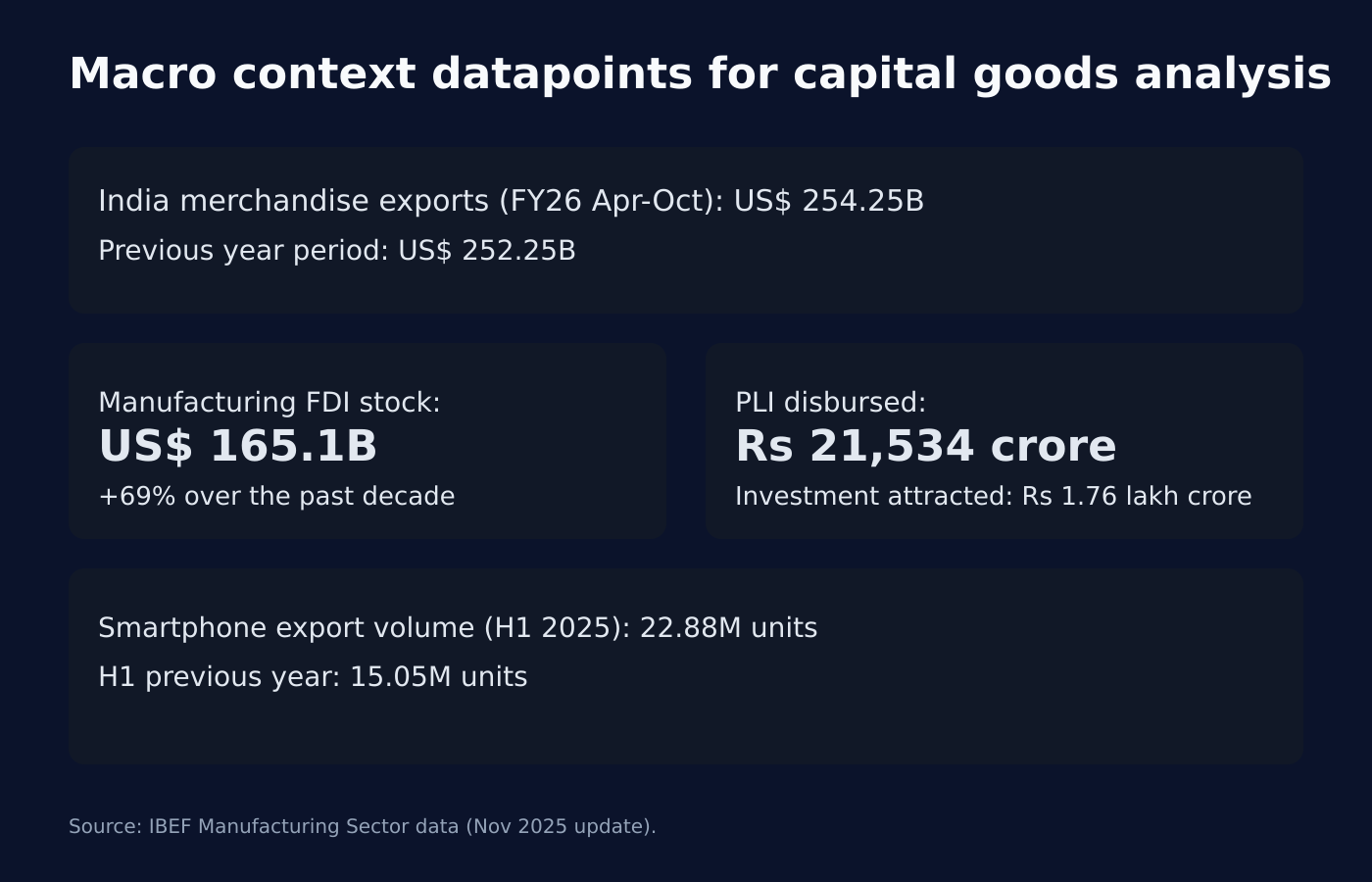

Macro context behind this cycle

| Indicator | Latest value used | Why it matters for capital goods |

|---|---|---|

| India merchandise exports (FY26 Apr-Oct) | US$ 254.25B | Indicates broad manufacturing demand support |

| Previous-year same period exports | US$ 252.25B | Shows growth is present, but not overheated |

| Manufacturing FDI stock | US$ 165.1B | Supports medium-term demand for engineering and equipment |

| Manufacturing FDI growth (decade) | +69% | Signals structural investment direction |

| PLI disbursed (as of Mar 2025) | Rs 21,534 crore | Policy execution marker |

| Investment attracted under PLI | Rs 1.76 lakh crore | Capex mobilization signal |

| Smartphone exports volume (H1 2025) | 22.88M units | Proxy for manufacturing scale-up |

| Smartphone exports (H1 previous year) | 15.05M units | Useful growth comparison |

Source: IBEF Manufacturing Sector data (Nov 2025 update).

Why order-book headlines can mislead

A big order book is useful, but not enough. Returns usually disappoint when execution slows, margins weaken, or cash conversion deteriorates.

The right question is not “How big is the order book?” The right question is: “How much of this backlog can convert into healthy earnings and cash in the next 6-8 quarters?”

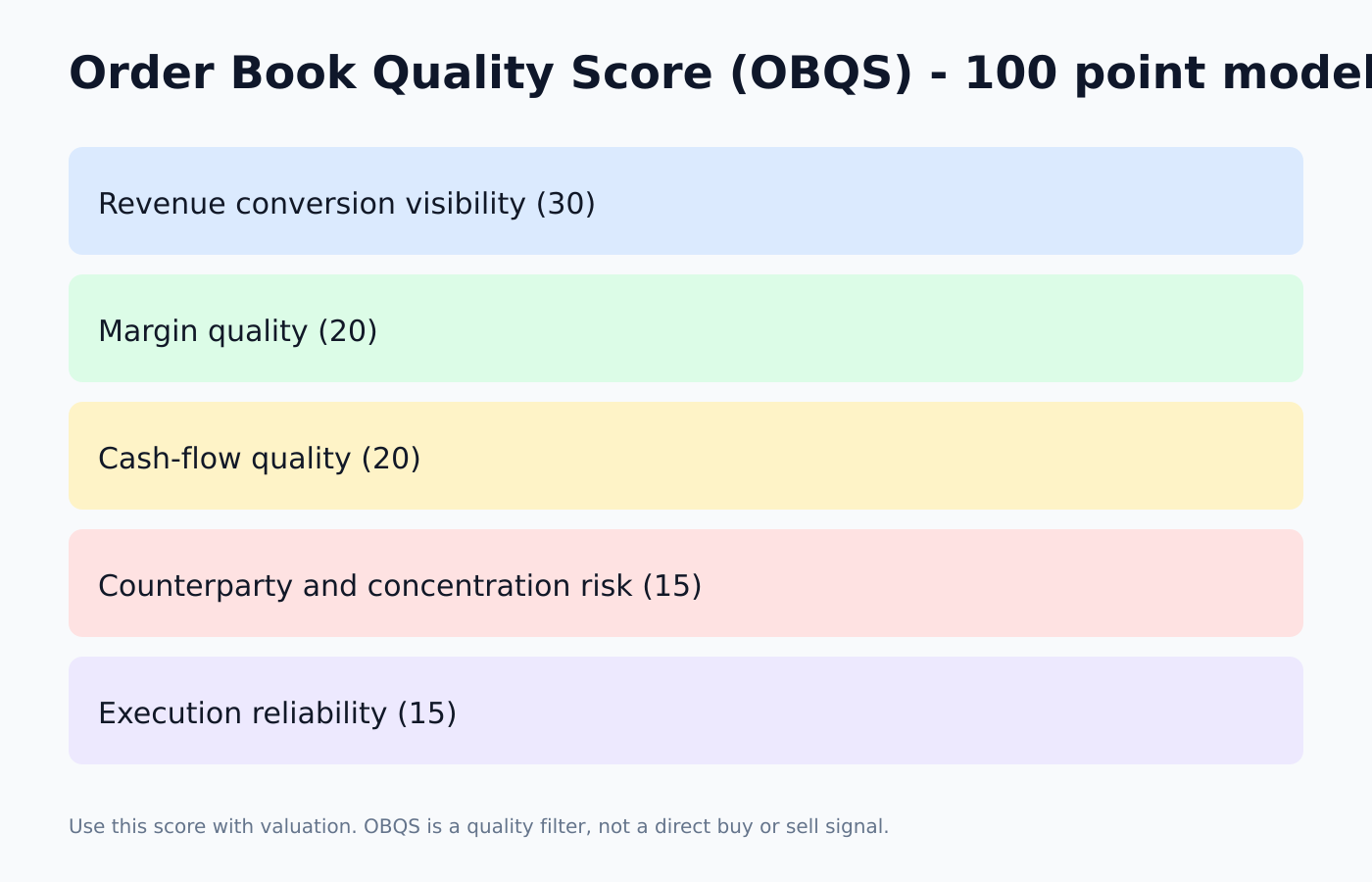

OBQS framework (100 points)

| OBQS component | Weight | What to track |

|---|---|---|

| Revenue conversion visibility | 30 | Book-to-bill trend, executable backlog share, conversion history |

| Margin quality | 20 | Contract mix, segment margin trend, pricing protection |

| Cash-flow quality | 20 | Receivable days, CFO/EBITDA trend, payment structure |

| Counterparty and concentration risk | 15 | Client concentration, public/private mix, export concentration |

| Execution reliability | 15 | Delay history, guidance credibility, completion consistency |

| Total | 100 | Quality score before valuation decision |

Score bands

| Score | Interpretation | Positioning bias |

|---|---|---|

| 80-100 | High-quality backlog profile | Core watchlist candidate |

| 60-79 | Mixed quality profile | Selective, valuation-sensitive |

| Below 60 | Weak quality support | Avoid or tactical only |

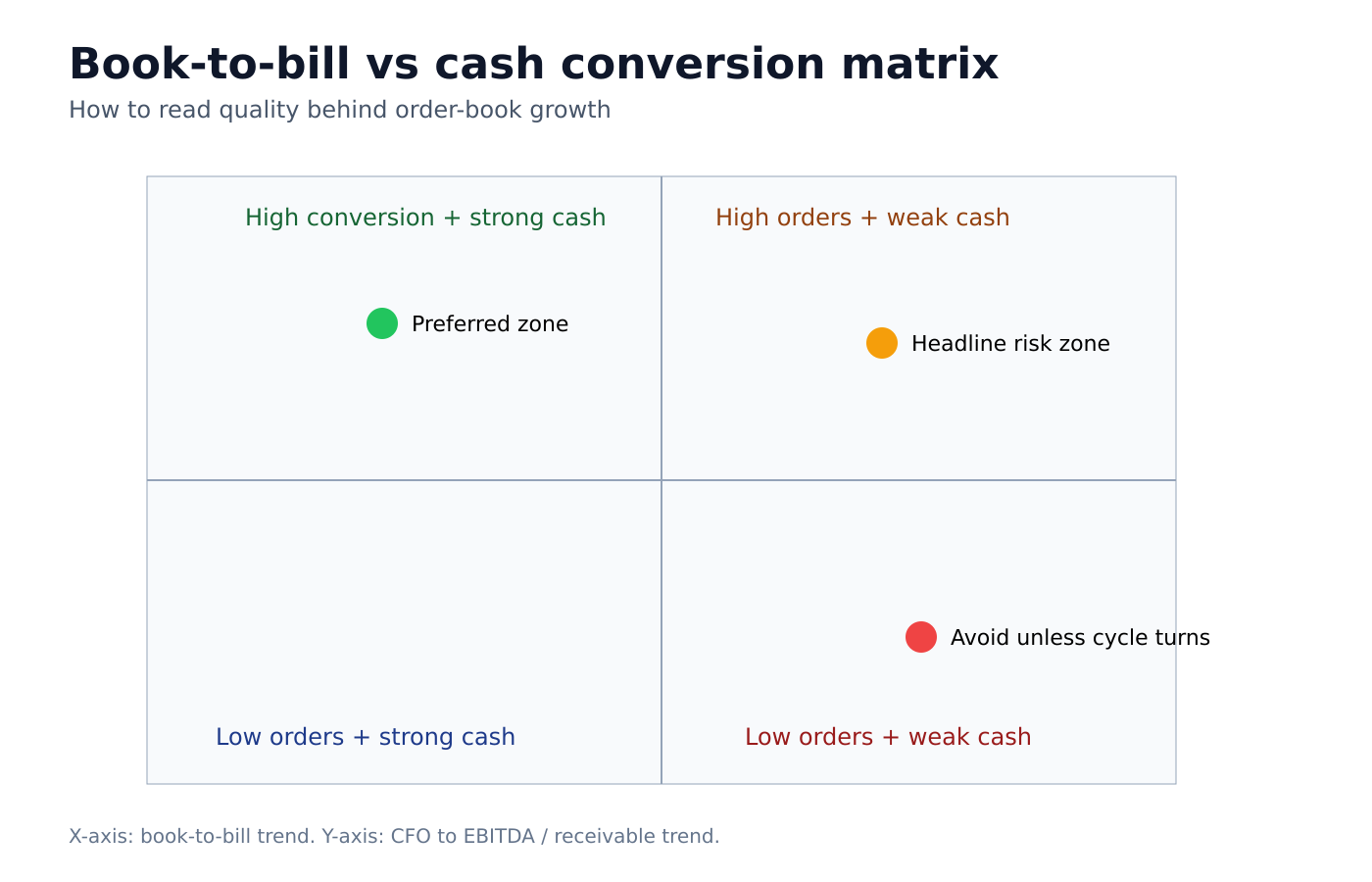

Book-to-bill must be read with cash conversion

| Book-to-bill trend | Cash conversion trend | Practical reading |

|---|---|---|

| Strong | Strong | Best quality zone |

| Strong | Weak | Headline-risk zone |

| Weak | Strong | Defensive quality, lower growth |

| Weak | Weak | Avoid unless turnaround evidence appears |

Company-level fields to track every quarter

| Field | Why it matters |

|---|---|

| Opening and closing order book | Backlog direction |

| Order inflow | Demand momentum |

| Revenue execution | Conversion progress |

| Book-to-bill | Cycle intensity |

| Receivable days | Cash stress signal |

| Working capital days | Balance-sheet pressure |

| CFO/EBITDA | Earnings quality check |

| Segment margins | Mix quality |

| Guidance vs delivery | Management reliability |

Red flags for the next two quarters

- Order growth with receivable stretch

- EBITDA growth not converting into CFO

- Rising share of long-dated backlog

- Margin pressure in fixed-price projects

- Valuation expansion without quality improvement

Scenario view

| Scenario | What needs to happen | Likely market response |

|---|---|---|

| Bull | Strong inflow + clean execution + stable receivables + margin hold | Rerating with upgrades |

| Base | Healthy inflow + moderate delays + mixed cash conversion | Range-bound, selective upside |

| Bear | Execution slippage + receivable stress + margin compression | Derating despite headline backlog |

Practical checklist before taking exposure

- Is executable backlog share improving?

- Are receivable days stable?

- Is CFO quality supporting EBITDA?

- Is contract mix margin-safe?

- Is valuation fair for current quality?

If two or more answers are weak, position size should be conservative.

FAQ

Is a large order book always bullish?

No. It helps only when execution and cash conversion stay healthy.

Most useful quality check?

Receivable trend + CFO/EBITDA trend together.

Why is valuation risk high in early capex cycles?

Because markets often price delivery before delivery is visible.

How often should this be updated?

Quarterly after results, with monthly tracking for major order and execution updates.

Related read: if you are tracking grid-linked execution risk, read our India Power T&D execution bottlenecks playbook.

Share this insight

Spread the Alpha

Related Articles

More ideas that align with your trading playbook.

India’s Crude Sensitivity Ladder: 10 Stocks to Watch if Brent Holds Above $120

If Brent holds above $120, Indian equities are unlikely to react in one wave. This crude sensitivity ladder ranks 10 stocks to…

Personal Finance Risk Checklist for Indian Investors: Before You Increase Equity Exposure

The first risk in equity investing is not volatility. It is interruption. A strong portfolio needs time, cash-flow stability, and a household…

Make in India Stocks Valuation: Theme vs Fundamentals Reality Check (2026)

The Make in India manufacturing story is real. The valuation story is where things get tricky. In parts of the capex basket,…

DailyBulls (Arthashilpi Ventures) is a D-U-N-S verified company.

DailyBulls (Arthashilpi Ventures) is a D-U-N-S verified company.