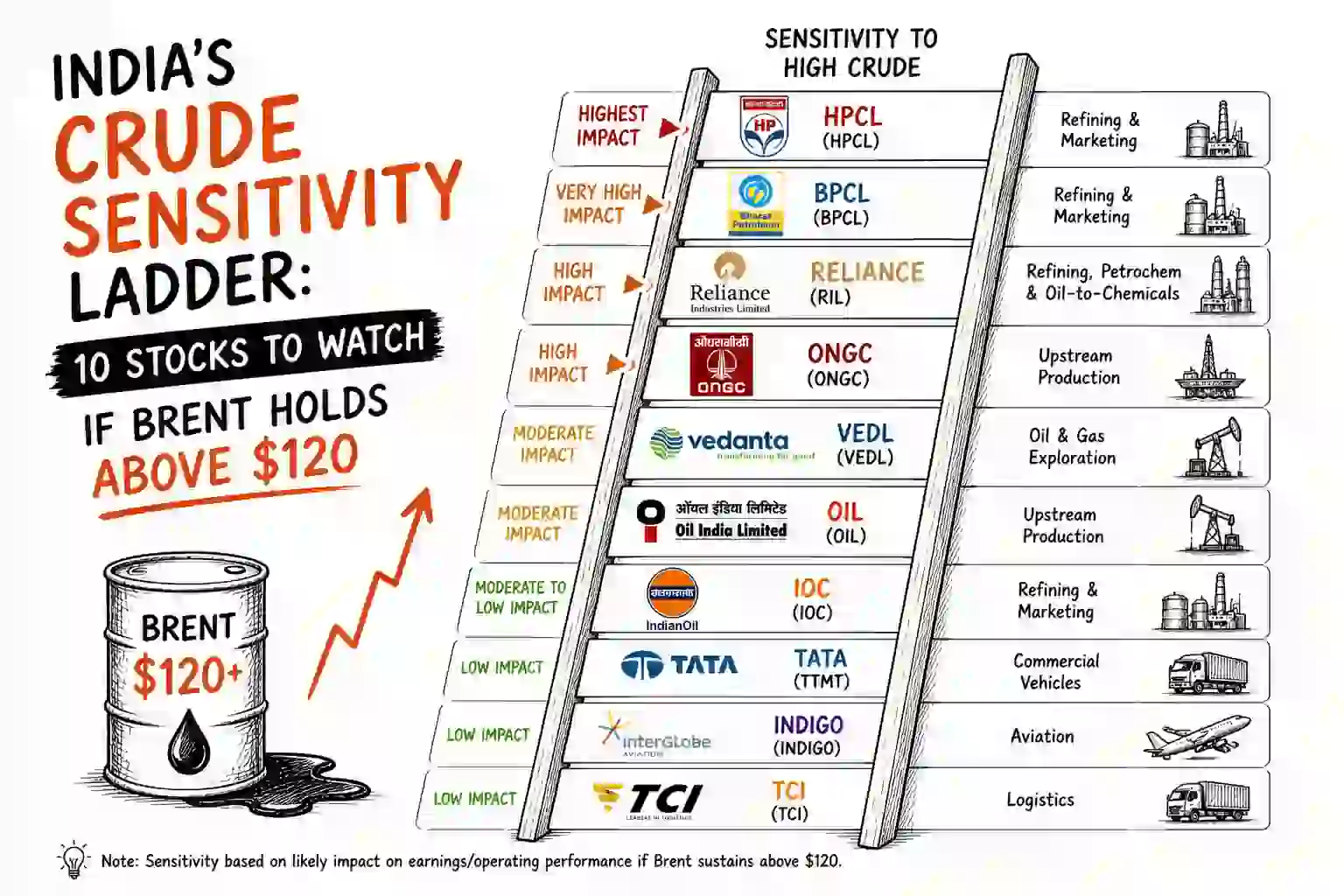

India’s Crude Sensitivity Ladder: 10 Stocks to Watch if Brent Holds Above $120

If Brent holds above $120 for two weeks, the market will stop treating it like a headline spike and start treating it like a condition. That distinction matters. A short oil burst can be ignored, faded, or blamed on geopolitics. A persistent $120-plus regime is different because it begins to alter earnings assumptions, rupee expectations, bond yields, and sector leadership.

That is why a stock watchlist is more useful than a broad macro opinion here. Indian equities are unlikely to sell off in one uniform move. They tend to reprice in sequence. The names with direct fuel or feedstock exposure usually react first. The companies linked to broader macro tightening usually react later.

Here is a practical crude sensitivity ladder for Indian markets if Brent stays above $120.

Tier 1: The first responders to a crude shock

These are the names where the market usually starts repricing early because the transmission channel is visible and immediate.

1) InterGlobe Aviation

This is the cleanest direct crude-sensitivity stock in the Indian market. Aviation fuel is one of the largest variables in the cost structure, and the market usually responds quickly when Brent stays elevated long enough to threaten margin assumptions.

What to watch:

- whether airline stocks underperform even on flat index days

- whether the market starts discounting weaker near-term margins before management commentary catches up

- whether fuel-cost worries begin to overpower traffic-growth optimism

2) Indian Oil Corporation

IOC sits near the front of the ladder because oil marketing companies get repriced not just on crude direction but on uncertainty around retail pricing, inventory effects, and refining-marketing margin expectations. In a prolonged oil spike, the market starts questioning how much cost can be passed through cleanly.

What to watch:

- relative performance versus the broader OMC basket

- any signs that pricing flexibility may narrow

- whether investors shift focus from valuation comfort to policy and margin risk

3) Bharat Petroleum

BPCL belongs in the same early bucket for similar reasons, but traders should still watch basket behavior rather than treating all OMCs as identical. If Brent stays above $120, the question is not just whether crude is high. It is whether downstream names remain investable when cost pass-through becomes politically and operationally less straightforward.

What to watch:

- whether BPCL weakens alongside IOC and HPCL rather than diverging on company-specific factors

- whether refining optimism stops offsetting fuel-price stress

- whether the market begins pricing in a tougher earnings mix

4) Hindustan Petroleum

HPCL is another first-wave stock because the market tends to move early on perception, not after a complete quarterly reset. If the oil shock looks persistent, OMCs can reprice before the accounting detail becomes visible.

What to watch:

- whether HPCL becomes the weaker link in the OMC basket

- whether pressure broadens on days when crude and the rupee both move the wrong way

- whether the stock stops responding to market rebounds

5) Apollo Tyres

Tyre companies do not have the same instant headline sensitivity as airlines, but they still sit close to the front of the ladder because crude-linked input costs matter enough to trigger margin concerns. A sustained oil move can quickly change how the market thinks about cost pressure in the next few quarters.

What to watch:

- whether tyre stocks begin underperforming even without broader market stress

- whether margin-sensitive names get sold ahead of results

- whether input-cost anxiety spreads across the tyre basket

Tier 2: The second wave, input-cost and cyclical spillover

These stocks may not be the first to break, but they become vulnerable once the market accepts that elevated crude is feeding into a broader cost and demand problem.

6) Asian Paints

Paint companies are not pure oil trades, but they are too exposed to petrochemical-linked input costs to be ignored in a prolonged Brent shock. If crude remains elevated, the market starts thinking less about brand strength and more about gross-margin pressure.

What to watch:

- whether premium consumer defensives start losing their relative safety status

- whether earnings-quality discussions shift toward input inflation

- whether the market becomes less willing to pay a premium multiple into cost pressure

7) SRF

SRF is worth watching because it sits closer to the chemical and industrial feedstock side of the transmission chain. The exact earnings effect is more complex than a simple crude-up, stock-down formula, but this is exactly why it belongs in the middle of the ladder. If energy-linked inputs and global demand both turn less friendly, the stock can become more fragile than broad market narratives suggest.

What to watch:

- whether margin worries begin outrunning business-quality arguments

- whether the chemical basket weakens alongside rising energy costs

- whether investors start prioritizing spread compression risk

8) Hindalco Industries

Metals are a second-order oil shock trade, not a first-order one. That is what makes Hindalco useful on the ladder. A weak rupee can help export-linked businesses at the margin, but that benefit can get diluted if energy costs remain high and global growth expectations soften.

What to watch:

- whether metals stop behaving like cyclical beneficiaries and begin trading like macro casualties

- whether the rupee tailwind fails to support sentiment

- whether global growth worries start overpowering any currency advantage

Tier 3: The macro confirmation layer

Once oil pressure spreads from sector pain into inflation, yields, and financial conditions, the market usually tests private banks next. This is where the oil story becomes more serious.

9) Axis Bank

Axis Bank is not directly crude-sensitive, but it becomes important when the oil shock starts influencing yields, liquidity expectations, and broad risk appetite. If Brent holds above $120 and Bank Nifty starts lagging, private lenders like Axis Bank become a useful read on whether the market is shifting from sector stress to macro repricing.

What to watch:

- whether Bank Nifty underperforms Nifty during rebounds

- whether private lenders lose leadership while crude-sensitive sectors are already weak

- whether the market starts discussing funding conditions and valuation compression together

10) HDFC Bank

HDFC Bank belongs on this list not because it should fall first, but because it helps confirm whether the repricing is becoming structural. If one of the market’s core leadership names starts losing relative strength in an oil-driven macro scare, that is usually a signal that the shock is broadening beyond the obvious losers.

What to watch:

- whether large private banks stop attracting defensive institutional flows

- whether yield pressure starts feeding into valuation caution

- whether the weakness begins to look sector-wide rather than stock-specific

How to read the ladder properly

This is not a list of guaranteed losers. It is a sequencing framework.

If Brent stays above $120 but the rupee stabilizes and Indian bond yields remain contained, the market may keep the damage concentrated in the first bucket, mainly airlines, OMCs, and selected input-cost names.

If Brent stays high and the rupee remains weak, the second bucket becomes more vulnerable. That is when paints, chemicals, and metals start feeling less like stock stories and more like macro stories.

If Brent stays high, the rupee weakens further, and the 10-year yield remains above 7 percent while Bank Nifty lags, then the third bucket matters much more. At that point, the market is no longer pricing an oil move. It is pricing tighter financial conditions.

The real signals to track

If you want to use this crude sensitivity ladder properly, do not watch stock charts in isolation. Track the chain.

Focus on:

- Brent holding above $120 for multiple sessions

- USD/INR staying under pressure

- India 10-year yield remaining elevated

- Bank Nifty lagging Nifty

- broad weakness across airlines, OMCs, tyres, and selected cyclicals

If those signals line up together, the watchlist becomes more actionable. If they diverge, the move may still be headline-driven rather than durable.

That is the real edge here. A persistent oil shock does not hit all Indian stocks at once. It tends to climb a ladder. First the direct fuel and feedstock names. Then the cost-sensitive cyclicals. Then the financials that confirm whether macro stress is turning structural.

If Brent holds above $120, that sequence is what traders should watch, not just the headline price of crude.

Not investment advice. Always do your own research before trading.

Share this insight

Spread the Alpha

Related Articles

More ideas that align with your trading playbook.

Personal Finance Risk Checklist for Indian Investors: Before You Increase Equity Exposure

The first risk in equity investing is not volatility. It is interruption. A strong portfolio needs time, cash-flow stability, and a household…

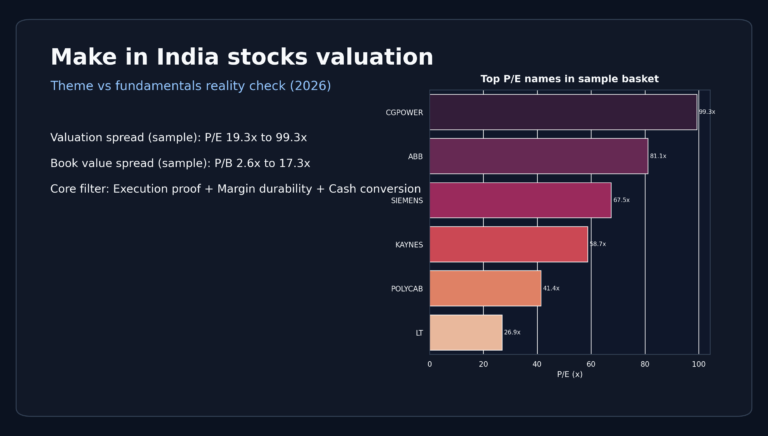

Make in India Stocks Valuation: Theme vs Fundamentals Reality Check (2026)

The Make in India manufacturing story is real. The valuation story is where things get tricky. In parts of the capex basket,…

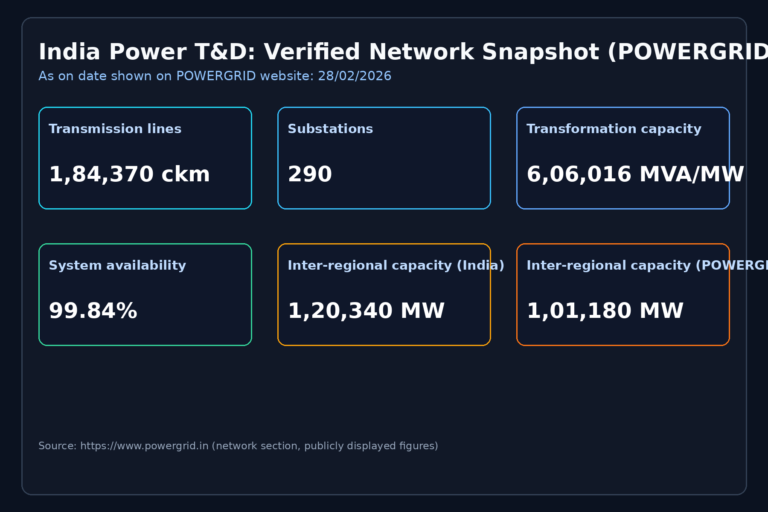

India Power T&D Execution Bottlenecks: Investor Playbook (2026)

Quick take The india power t&d execution bottlenecks story is simple: the capex runway is large, but returns depend on execution quality,…

DailyBulls (Arthashilpi Ventures) is a D-U-N-S verified company.

DailyBulls (Arthashilpi Ventures) is a D-U-N-S verified company.