India’s Data Center Power Trade: Which Stocks Benefit First if AI Infra Spending Accelerates?

India’s AI buildout is easy to describe as a digital theme. It sounds like a story about cloud software, chips, and futuristic applications. But if you want to understand the India data center power trade stocks that may actually move first, the more useful lens is physical infrastructure.

That is because large AI-ready data centers are not ordinary commercial buildings. They require stable power, backup layers, grid interconnection, industrial cabling, thermal management, and increasingly more sophisticated cooling. In other words, before the market can obsess over who owns the server halls, it usually has to deal with the companies that make those facilities electrically and thermally possible.

That is the real investment angle here. If AI infra spending accelerates in India, the first listed beneficiaries may not be the direct data-center landlords. They may be the transformer, switchgear, conductor, cable, backup-power, and cooling names that sit closer to the bottlenecks.

Why this is becoming a power trade, not just an AI trade

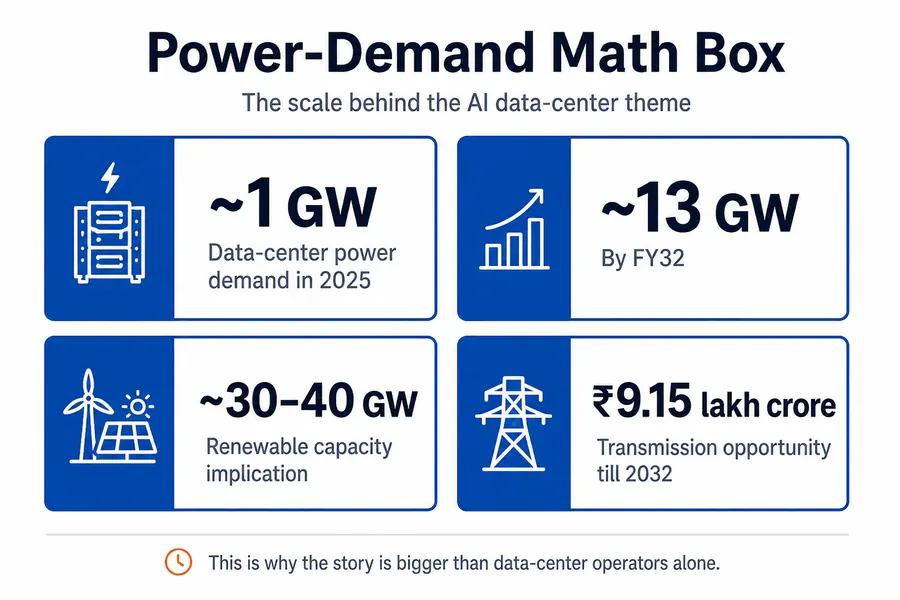

The demand backdrop is already meaningful enough to matter. India’s operational data-center capacity is widely cited around 1.4-1.5 GW in 2025, versus a much smaller base a few years ago. Multiple reports now point to a multi-gigawatt path by 2030, and the more aggressive projections imply that the next phase of growth could be shaped by AI workloads rather than ordinary enterprise demand.

The more important number is power demand. Recent reporting cited data-center electricity demand rising from roughly 1 GW in 2025 to 13 GW by FY32. If that kind of trajectory begins to look realistic, the market will not treat data centers as just another real estate or telecom sub-theme. It will start treating them as a serious load-creation story for the grid, for transmission, for electrical equipment, and for cooling.

That is why this theme deserves a stock ladder rather than a broad macro opinion. Indian equities are unlikely to price it in one wave. They are more likely to reprice in sequence, starting with the companies closest to the non-negotiables.

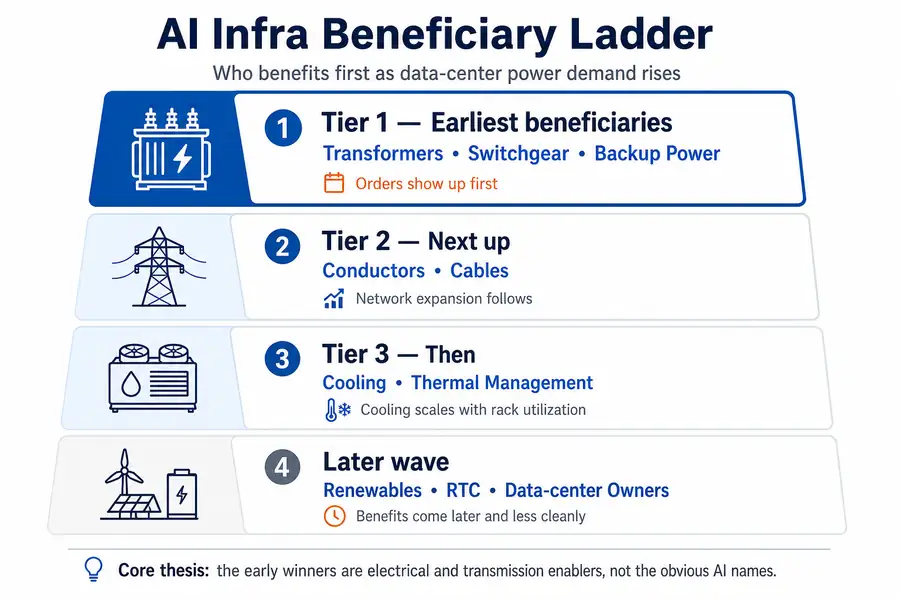

Tier 1: The first-order beneficiaries

These are the names that should benefit first if AI infra spending turns into visible order flow. The reason is simple. Every serious data-center campus needs power architecture before utilization ramps. Transformers, switchgear, substations, backup systems, and industrial-grade electrical infrastructure are not optional upgrades. They are prerequisite capex.

1) Hitachi Energy India

If this theme gets real, Hitachi Energy India is one of the cleanest names to watch. The company sits near the center of high-voltage equipment, grid interconnection, and power-quality infrastructure, all of which become more critical when hyperscale facilities concentrate large and continuous loads.

What to watch:

- stronger commentary around transformer, grid, or substation demand

- signs that load-heavy digital infrastructure is becoming part of the order narrative

- continued strength in power-transmission linked capex visibility

2) ABB India

ABB India belongs near the front of the ladder because it is tied to electrification, switchgear, automation, and power-management capabilities that become increasingly valuable as uptime requirements rise. AI-ready data centers do not just need electricity. They need reliable and well-managed electricity.

What to watch:

- whether the market begins rewarding ABB more as a power-quality and infrastructure enabler than as a broad industrial name

- management commentary around electrification intensity and digital infrastructure demand

- order visibility from mission-critical facilities

3) Siemens India

Siemens India is another early beneficiary candidate because it sits inside the same broad power-enablement layer. If the Indian market starts treating AI infra as a physical buildout theme, Siemens can become part of that conversation through its electrical equipment and industrial infrastructure exposure.

What to watch:

- whether power-equipment names begin outperforming broader industrials

- any signal that digital infrastructure is entering customer discussions more directly

- sustained rerating of electrical-capex beneficiaries

4) CG Power

CG Power is harder for the market to ignore in this theme because it has already been a visible beneficiary of India’s broader electrical-capex cycle. If AI infra becomes another accelerant, the stock could be treated as a practical, execution-linked way to play transformer and electrical-equipment demand rather than as a conceptual AI story.

What to watch:

- whether the market begins treating data-center power demand as an incremental leg of the existing capex cycle

- fresh interest in transformer and heavy-electrical names as data-center coverage increases

- continued order-book confidence across infrastructure-linked segments

5) Cummins India

Cummins India may not be the first name that comes to mind in an AI discussion, which is exactly why it is interesting. Data centers require redundancy. Backup power is not decorative. It is a core reliability layer. If campus-scale AI infrastructure expands, the relevance of backup-generation systems should remain high even as renewable and storage integration improves over time.

What to watch:

- whether the market starts revisiting backup-power suppliers as part of the data-center theme

- commentary tied to mission-critical infrastructure demand

- whether power-reliability narratives stay strong alongside grid-upgrade narratives

Tier 2: The conductor and cable layer

Once you move beyond transformers and switchgear, the next logical beneficiaries are the companies that help carry that power and connectivity. This is where the India data center power trade becomes more interesting, because a cable boom can ride both the direct data-center buildout and the broader transmission cycle developing around it.

6) Apar Industries

Apar sits in a strong position because it connects more directly to conductors and transmission infrastructure than many of the generic cable-theme names. If data-center demand intensifies pressure on the grid and evacuation network, Apar can benefit through the wider T&D build cycle, not just through a narrow data-center narrative.

What to watch:

- whether conductors and transmission accessories move higher in market discussions around AI infra

- continued momentum in T&D-related order expectations

- signs that localized load concentration near data-center hubs is sharpening the power-delivery case

7) Polycab India

Polycab is one of the most obvious organised cable proxies for this theme. Every large data-center project needs internal power cabling, electrical systems, and associated infrastructure. If India moves toward denser campuses and modular deployments, names like Polycab can benefit from both direct project intensity and broader institutional demand.

What to watch:

- whether the market starts treating industrial and infrastructure cable demand as a separate driver from consumer electrical demand

- stronger positioning of Polycab inside institutional-capex discussions

- relative strength versus other cable names when digital-infra headlines pick up

8) KEI Industries

KEI belongs in the same basket because it has meaningful exposure to institutional and infrastructure-grade cable demand. If AI infra spending accelerates, KEI may start getting mentioned less as a plain-vanilla cable company and more as part of the enabling layer behind data centers, transmission, and high-quality electrical installations.

What to watch:

- whether institutional order-book commentary grows more important than retail electrical narratives

- sustained re-rating across cable names as a group

- evidence that the market is pricing not just data creation, but the physical systems behind it

Tier 3: Cooling and thermal management, the underestimated layer

Many investors may understand the power angle before they understand the cooling angle. That may be a mistake. As rack density rises, cooling stops being a secondary systems story and starts becoming a bottleneck story. If AI workloads expand faster, cooling may become one of the cleaner second-wave trades in the theme.

9) Blue Star

Blue Star is worth watching because it gives the market a listed way to participate in precision cooling, project execution, and thermal-management demand without forcing investors to chase direct data-center developers. If AI-driven heat intensity becomes part of the mainstream narrative, Blue Star may benefit from both revenue visibility and thematic rerating.

What to watch:

- management commentary around data-center cooling demand

- signs that higher-margin project mix becomes part of the market story

- whether the cooling segment begins to command more investor attention than traditional HVAC framing

10) Voltas

Voltas rounds out the ladder because its project and cooling exposure gives it a practical angle into the same thermal-management theme. If the market starts recognizing that AI facilities require more than ordinary air-conditioning, Voltas can become part of that repricing through execution capability and specialised cooling relevance.

What to watch:

- whether data-center cooling is discussed as a differentiated order opportunity

- evidence that energy-efficient or advanced cooling systems become a stronger growth talking point

- whether cooling names begin outperforming broader building-services peers

Why the market may get this theme wrong at first

The instinctive retail trade may be to chase the most obvious names, usually the companies directly announcing data-center campuses, AI ambitions, or hyperscaler partnerships. But that can be a noisy way to play the theme.

The cleaner first-order trade may sit lower in the stack.

That is because data-center owners and large conglomerates can absorb the theme inside much larger businesses. The impact can get diluted by capital structure, funding needs, execution timelines, or unrelated business segments. The enabling layer is often less glamorous, but it is also often closer to real order flow.

This is why the first market winners may emerge from the boring parts of the chain. Transformers, switchgear, conductors, industrial cables, backup power, and cooling may all look less exciting than AI branding. But they are easier to monetize when the physical buildout begins.

Who may benefit later, but less cleanly

That does not mean the second-wave names are unimportant. They are still part of the theme. They are just not necessarily the earliest or cleanest way to express it.

The broader watchlist here includes:

- Power Grid

- Adani Energy Solutions

- Tata Power

- JSW Energy

- Tata Communications

- RailTel

- KRN Heat Exchanger

- Adani Enterprises

- Reliance Industries

- Lodha Developers

These names matter for different reasons. Some are tied to transmission, some to renewable or round-the-clock power supply, some to connectivity, and some to direct data-center ownership or shell infrastructure. But the market may take longer to isolate the specific AI infra contribution in these businesses, which is why they may not benefit first in a sharp repricing.

What would confirm that this trade is becoming real

If you want to track this theme properly, do not just watch flashy AI announcements. Watch the bottlenecks.

Focus on:

- fresh hyperscaler or large campus expansion announcements in India

- rising discussion around power density, redundancy, and cooling requirements

- signs that grid, substation, transformer, and transmission capex around data-center hubs is getting more urgent

- stronger commentary from electrical-equipment and cooling management teams

- more evidence that renewable, storage, and round-the-clock power contracts are being structured around digital loads

If those signals begin lining up together, the market will be more likely to treat this as a full infrastructure theme rather than a headline technology theme.

That is the real takeaway. India’s AI buildout may sound like a software story, but the first listed winners could come from the physical systems that make that buildout possible. If AI infra spending accelerates, the earliest stocks to reprice may not be the companies promising to own data centers. They may be the companies supplying the power, cables, redundancy, and cooling that let those data centers actually run.

Not investment advice. Always do your own research before trading.

Share this insight

Spread the Alpha

Related Articles

More ideas that align with your trading playbook.

Reliance AGM 2026 Highlights: Jio IPO, AI and New Energy Plans Explained

Reliance Industries’ annual general meetings usually come with big announcements. The 2026 AGM was no different. But beneath the new products, ambitious…

SEBI’s Commodity Plan Just Lost Its Institutional Anchor. What It Means for MCX

SEBI wanted banks, insurers, and eventually pension funds to deepen India's commodity derivatives market. RBI and IRDAI are not inclined to allow…

If Brent Holds Above $120 for 2 Weeks, Which Indian Sectors Reprice First?

A one-day crude spike can be ignored. Two weeks above $120 Brent is different. At that point, Indian markets stop treating oil…

DailyBulls (Arthashilpi Ventures) is a D-U-N-S verified company.

DailyBulls (Arthashilpi Ventures) is a D-U-N-S verified company.