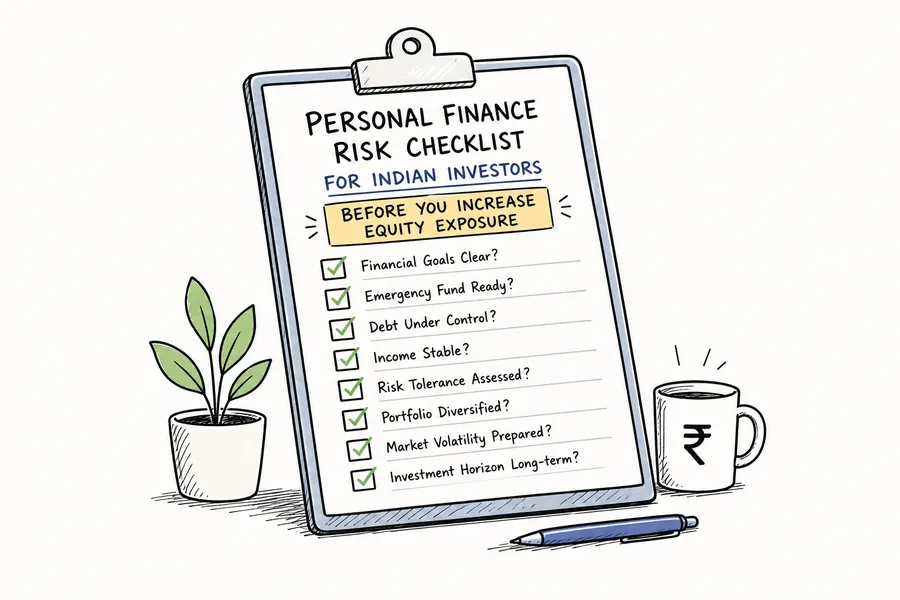

Personal Finance Risk Checklist for Indian Investors: Before You Increase Equity Exposure

The first risk in equity investing is not volatility. It is interruption.

A strong portfolio needs time, cash-flow stability, and a household balance sheet that can survive difficult months without forcing a bad sell decision. That is why a personal finance risk checklist should come before a higher SIP, a fresh small-cap allocation, or a bigger thematic bet.

Before taking more equity risk, investors should check whether the basics are in place: emergency liquidity, adequate insurance, manageable debt, sustainable cash flow, and clear goal protection. These layers do not replace investing. They make it easier to stay invested when life becomes unpredictable.

Why This Matters Now

Indian households are committing more money to market-linked products through SIPs, mutual funds, direct equity, and thematic investing. This is positive for long-term wealth creation, but it also means more household wealth is now exposed to market cycles.

The problem is that many investors evaluate companies more carefully than they evaluate their own financial base. They look at business quality, valuations, sector cycles, earnings growth, and market themes. But they may not check whether their own household can handle a medical emergency, job loss, EMI pressure, or income disruption.

Investors often spend time separating market narratives from actual fundamentals, as discussed in our article on theme vs fundamentals. The same discipline should also apply to personal finances before increasing equity exposure.

A portfolio is designed to build wealth over time. It should not be forced to act as your emergency fund, hospital-bill reserve, loan-repayment backup, and family income replacement plan all at once.

The Core Problem: Portfolios Often Break Because Life Interrupts

Most investors think portfolio risk means market risk.

But in real life, portfolios often get disturbed because of non-market events:

- A sudden medical expense

- Job loss or income disruption

- High EMI pressure

- Family dependency

- Poor tax planning

- Lack of emergency savings

- No income protection for dependents

These events can force investors to redeem mutual funds, sell stocks at the wrong time, stop SIPs, or take expensive debt.

That is why the first job of personal finance is not return maximisation. It is survival. Once survival risk is handled, investors are in a much better position to take long-term market risk.

The 7-Part Personal Finance Risk Checklist

1. Emergency Liquidity

Before increasing equity exposure, ask a simple question: how many months can your household run without selling long-term investments?

For most salaried investors, six months of essential expenses is a sensible starting point. Single-income households, self-employed professionals, business owners, and families carrying heavy EMIs may need a larger buffer.

This money is not meant to chase high returns. It is survival capital. Its job is to stop a temporary cash-flow problem from becoming a permanent portfolio mistake.

A large portfolio number is useful only if the household also has enough liquidity to avoid forced selling. Cash availability, debt pressure, insurance cover, and income stability matter as much as the portfolio value shown on an app.

2. Health Insurance Adequacy

A portfolio should not be your default hospital-bill payer.

A major medical expense can damage years of savings if the household is not properly covered. Many investors assume employer health insurance is enough. But employer cover may be limited, may not fully cover all family members, and may not continue if the job changes.

Health insurance is not just a medical product. For investors, it is also a portfolio-protection tool.

Before increasing equity exposure, check:

- Do you have your own health insurance apart from employer cover?

- Is the sum insured enough for your city and family size?

- Are parents separately covered?

- Are room-rent limits, exclusions, and waiting periods clear?

- Does the policy have a good hospital network?

- Are you depending only on savings to handle medical emergencies?

The core point is simple: health cover reduces the chance that your portfolio gets disturbed by a medical shock.

3. Income Protection

If your family depends on your earnings, the biggest risk in your financial plan is not a bad quarter in the market. It is the permanent loss of income.

Your portfolio may look strong today. Your SIPs may be running. Your long-term goals may be mapped. But if the household depends on one person’s income, then the entire plan depends on that income continuing.

If that income stops permanently, the portfolio may not have enough time to grow.

This is where term insurance becomes relevant. Unlike investment-linked insurance products, it is designed mainly for income protection. If the insured person passes away during the policy term, the family receives a payout that can help cover living expenses, loans, children’s education, and other long-term responsibilities.

For an investor, income protection can help protect:

- Family living expenses

- Outstanding home loan or other liabilities

- Children’s education goals

- Spouse’s financial independence

- SIPs that were supposed to continue for years

- Long-term household stability

The mistake is treating term insurance as a return product. It should be treated as a risk-management layer.

4. Choosing Term Cover Carefully

Once the need for term cover is clear, the next step is not to choose the cheapest plan blindly.

A suitable term plan should be evaluated on multiple factors: insurer reliability, claim record, premium affordability, policy term, payout options, rider usefulness, exclusions, and the family’s actual financial responsibilities.

The right cover amount also matters. A random ₹50 lakh or ₹1 crore policy may look large, but it may not be enough if the family has a home loan, young children, long-term education goals, and many years of income dependency ahead.

Investors should compare plans with the same seriousness they use while comparing financial products. A shortlist of the best term plans in India should still be judged against the family’s actual needs, not just the premium shown on the screen.

5. Debt Pressure and Tax Drag

Debt changes an investor’s risk profile.

An investor with low debt and strong savings can usually handle market volatility better than someone with high EMIs, low liquidity, and aggressive equity exposure.

Not all debt is bad. A manageable home loan can be part of a financial plan. But expensive personal loans, credit card rollover, lifestyle EMIs, and high EMI-to-income ratios can weaken the household balance sheet.

Before increasing equity exposure, ask:

- What percentage of monthly income goes toward EMIs?

- Are you carrying credit card debt?

- Are personal loans being used to fund lifestyle spending?

- Can you continue SIPs if income falls temporarily?

- Would you need to sell investments if a large expense appears?

A useful EMI-risk guide:

| EMI Situation | Risk Level |

|---|---|

| EMI below 25–30% of monthly income | Comfortable |

| EMI around 35–45% | Needs caution |

| EMI above 50% | High stress |

| Credit card rollover or personal loans | Red flag |

High EMI pressure reduces your ability to stay invested during market corrections. It also makes investors emotionally weaker during volatility because every market fall starts feeling like a cash-flow threat.

Tax structure also matters because gross income is not the same as investible surplus. What matters is money left after tax, EMI, insurance premiums, household expenses, family obligations, and emergency savings.

Investors trying to understand their post-tax cash flow can also review our guide on the new tax regime, especially before increasing SIPs or equity exposure.

Before investing more, calculate your real monthly surplus.

Not the amount you hope to invest.

The amount you can invest without weakening the rest of your financial life.

6. SIP Continuity Risk

SIP calculators assume consistency.

They assume you will invest every month for 10, 15, or 20 years. But real life does not always work like that.

Income can fall. Bonuses can stop. Expenses can rise. Family responsibilities can increase. Markets can stay weak for long periods.

A SIP plan is only strong if you can continue it during difficult phases.

Before increasing SIP amounts, ask:

- Can I continue this SIP if income falls temporarily?

- Do I have enough emergency savings to avoid stopping investments?

- Are my insurance and debt obligations already handled?

- Am I increasing SIPs because markets are rising?

- Can I hold through a 20–30% correction without needing the money?

A smaller SIP that continues for 15 years is often better than an aggressive SIP that stops in the first bad year.

7. Goal Protection and Basic Housekeeping

Not every risk problem needs a new product. Some need better coordination.

Major goals should be mapped against actual liabilities, not just hoped-for returns. Home loan closure, school or college funding, spouse security, retirement planning, and parent support all need a named funding source.

Nominations should be updated. Insurance cover should reflect real obligations. Equity should be asked to do what it does well: compound over time, not rescue poor planning.

A strong financial plan does not depend on one product. It combines liquidity, insurance, debt control, investing discipline, and basic documentation.

Investor Safety Scorecard

| Risk Area | Green Zone | Caution Zone | Red Flag |

|---|---|---|---|

| Emergency fund | 6–12 months ready | 3–6 months | Less than 3 months |

| Health insurance | Personal/family cover beyond employer plan | Employer-heavy setup | No dependable cover |

| Term insurance | Cover linked to income, dependents, and liabilities | Basic cover not reviewed | No cover despite dependents |

| Debt burden | EMIs manageable | EMI pressure visible | High-cost debt or rollover |

| Tax and cash flow | Clear monthly surplus | Surplus fluctuates | Investing from stretched cash flow |

| SIP continuity | Can continue through stress | May need to reduce | Likely to stop quickly |

| Goal mapping | Liabilities and goals reviewed | Partially mapped | No clear backup plan |

If multiple areas are in the red-flag zone, the investor may need to strengthen the base before increasing market exposure.

Red Flags Before You Increase Equity Exposure

1. You Have No Emergency Fund

This is the biggest warning sign. Without emergency savings, even a small crisis can force you to sell investments. Equity should not be your first source of emergency liquidity.

2. You Depend Only on Employer Health Insurance

Employer cover is useful, but it may not be enough. It can change, stop, or prove insufficient during a major medical event.

3. You Have Dependents but No Income Protection

If your family depends on your income, the lack of term insurance can leave the entire financial plan exposed.

4. Your EMIs Are Already High

High fixed obligations reduce flexibility. They also make market volatility harder to handle emotionally.

5. You Are Increasing SIPs Because Markets Are Rising

A rising market can create confidence, but investment amounts should be based on cash-flow strength, not recent returns.

6. You Know Your Gross Salary, but Not Your Real Surplus

Investing decisions should be based on money left after tax, EMI, household expenses, insurance premiums, family obligations, and emergency savings.

7. You Have Not Reviewed Nominations and Beneficiaries

Good financial planning also requires basic housekeeping. Bank accounts, mutual funds, demat accounts, insurance policies, and retirement accounts should have updated nominations.

How to Think About Equity Exposure After This Checklist

The purpose of this checklist is not to scare investors away from equity.

Equity remains one of the most important asset classes for long-term wealth creation. But the ability to stay invested is often more important than the ability to find the perfect entry point.

A strong investor base usually looks like this:

- Emergency fund is ready.

- Health insurance is adequate.

- Term insurance is in place if there are dependents.

- High-cost debt is under control.

- Monthly surplus is clear.

- SIPs are sustainable.

- Goals and liabilities are mapped.

- Equity allocation is based on time horizon and risk capacity.

Once these layers are in place, market volatility becomes easier to handle.

The investor is no longer depending on the portfolio to solve every emergency. That makes it easier to stay invested through corrections, sideways markets, and temporary underperformance.

Practical Example

Consider two investors.

Both invest ₹25,000 per month. Both have similar income. Both hold mutual funds and direct stocks.

But Investor A has:

- No emergency fund

- Only employer health insurance

- No term insurance despite dependents

- High credit card debt

- SIPs that depend on every month going perfectly

Investor B has:

- 9 months of emergency savings

- Separate family health cover

- Term insurance linked to liabilities and family needs

- Manageable EMIs

- SIPs that can continue even during temporary stress

Both may earn similar market returns in a normal year.

But during a bad phase, Investor B has a much higher chance of staying invested. Investor A may be forced to stop SIPs, sell investments, or borrow at high interest.

That is the real difference.

Long-term wealth is not only built by choosing better investments. It is built by avoiding forced exits.

FAQs

Should I stop investing until all these areas are perfect?

Not necessarily. The goal is not perfection. The goal is balance.

You can continue investing while gradually strengthening your emergency fund, insurance cover, and debt position. But if multiple areas are weak, increasing equity exposure aggressively may not be wise.

Is health insurance more important than investing?

Both solve different problems.

Investing builds wealth. Health insurance protects wealth from medical shocks. A good financial plan usually needs both.

Is term insurance needed for everyone?

Term insurance is most relevant for people who have financial dependents, loans, or future family responsibilities. If nobody depends on your income and you have no major liabilities, the need may be lower.

How much emergency fund should investors keep?

Six months of essential expenses is a common baseline. But single-income families, business owners, freelancers, and people with high EMIs may need a larger buffer.

Should I increase SIPs every year?

You can, but only if your cash flow supports it. Do not increase SIPs only because markets are doing well. Increase them because your income, surplus, and financial base can support the commitment.

Should term insurance come before a higher SIP?

For investors with dependents, term insurance should usually be treated as a foundation layer. Wealth creation without income protection can leave the plan exposed if the main income source disappears.

Bottom Line

Good investing is not only about finding the right stock, fund, theme, or sector.

It is also about making sure life does not interrupt your compounding journey.

Before increasing equity exposure, check your emergency fund, health insurance, term insurance, debt burden, tax structure, SIP sustainability, and goal protection.

A strong portfolio needs a strong household balance sheet behind it.

And for most investors, that safety layer is the real first investment.

Share this insight

Spread the Alpha

Related Articles

More ideas that align with your trading playbook.

India’s Crude Sensitivity Ladder: 10 Stocks to Watch if Brent Holds Above $120

If Brent holds above $120, Indian equities are unlikely to react in one wave. This crude sensitivity ladder ranks 10 stocks to…

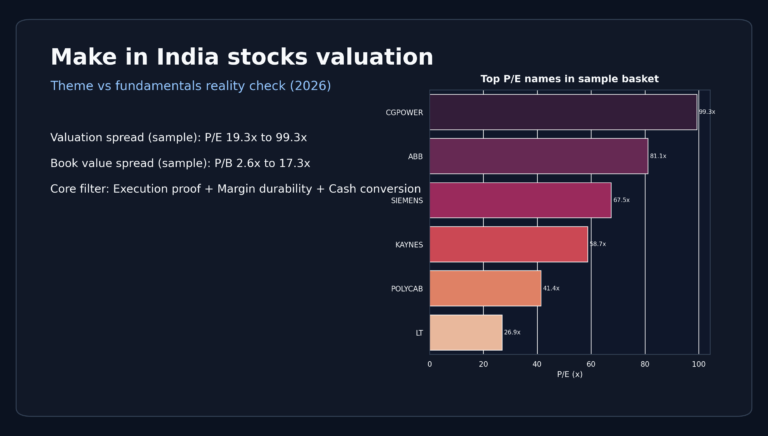

Make in India Stocks Valuation: Theme vs Fundamentals Reality Check (2026)

The Make in India manufacturing story is real. The valuation story is where things get tricky. In parts of the capex basket,…

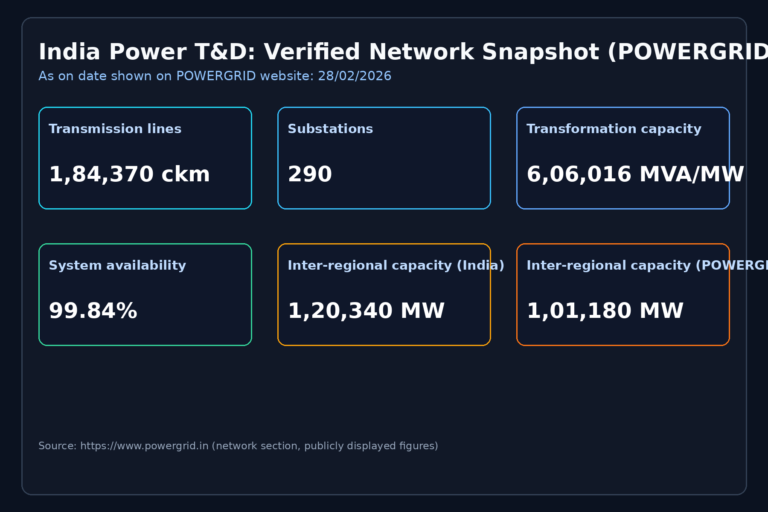

India Power T&D Execution Bottlenecks: Investor Playbook (2026)

Quick take The india power t&d execution bottlenecks story is simple: the capex runway is large, but returns depend on execution quality,…

DailyBulls (Arthashilpi Ventures) is a D-U-N-S verified company.

DailyBulls (Arthashilpi Ventures) is a D-U-N-S verified company.