Make in India Stocks Valuation: Theme vs Fundamentals Reality Check (2026)

The Make in India manufacturing story is real. The valuation story is where things get tricky.

In parts of the capex basket, prices are already assuming smooth execution for years. That can still work, but only if delivery, margins, and cash flow actually hold up. When valuation runs ahead of business proof, even strong themes can underperform.

That is exactly why a disciplined make in india stocks valuation framework matters now.

Quick take

- The theme is real, but valuation is highly uneven across the basket.

- Order announcements are only the start. Conversion into earnings and cash decides outcomes.

- P/E and P/B dispersion inside one theme is wide, so stock selection matters more than theme enthusiasm.

- Use a four-pillar check: execution, margins, cash conversion, and valuation discipline.

Why this matters now

At headline level, this cycle looks straightforward: policy push, capex expansion, multi-year opportunity. Markets, however, usually price the finish line before the middle of the race is visible.

So the key risk right now is not that the entire theme fails. The bigger risk is paying top-tier multiples before delivery quality is fully proven.

For broader cycle context, start with the Make in India 2.0 capex playbook. For execution-level filters, use the capital goods order book quality framework.

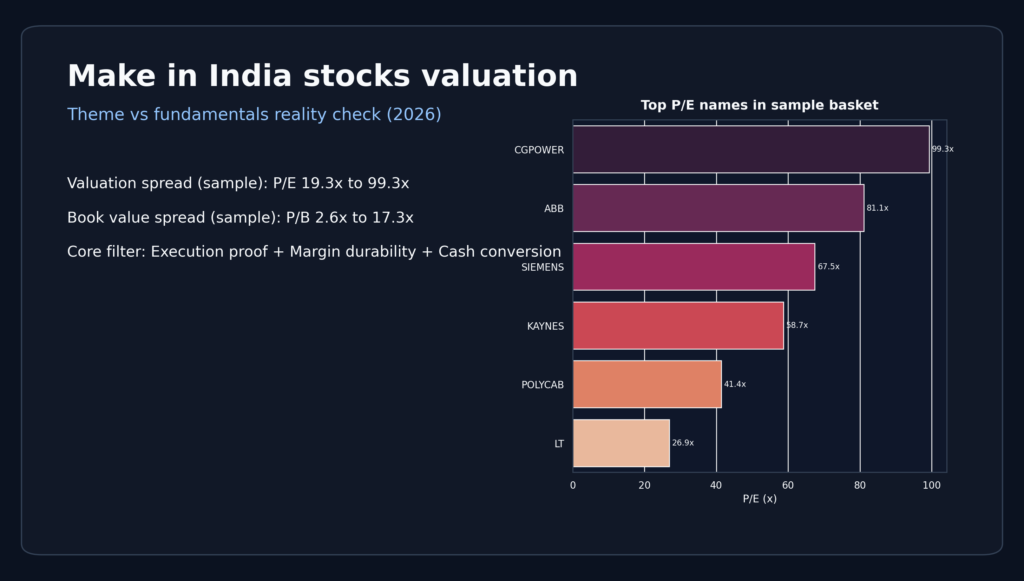

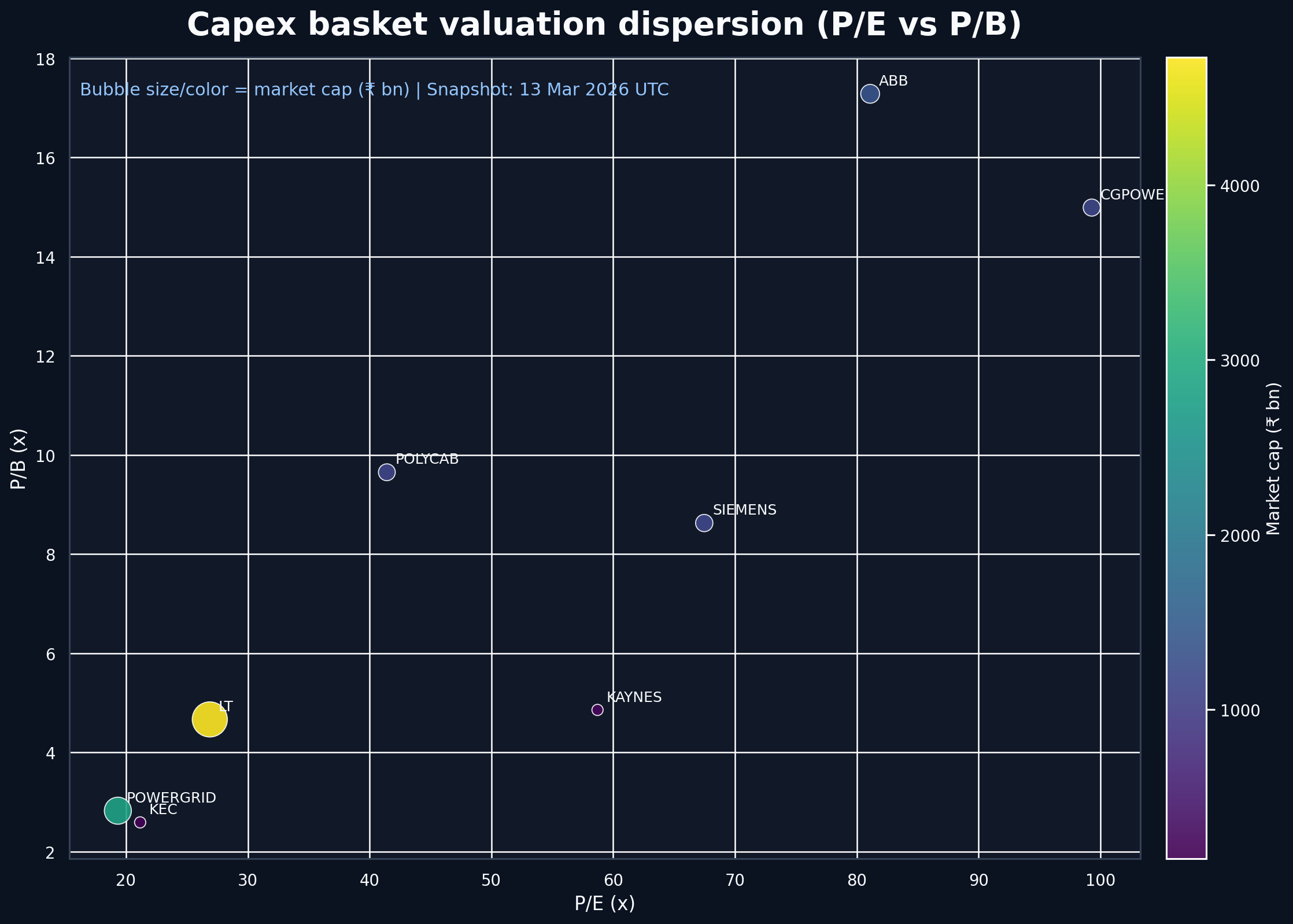

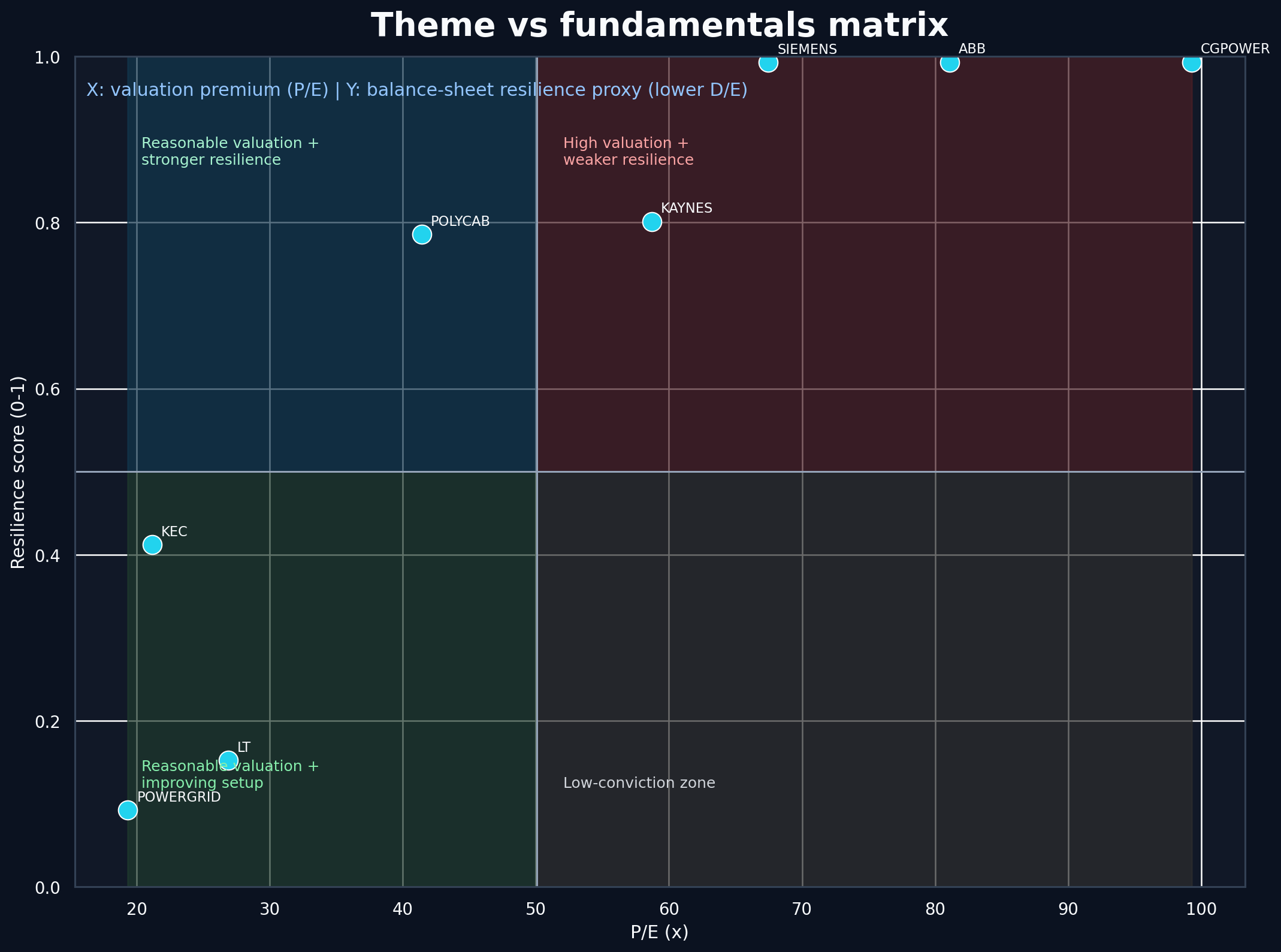

Data snapshot: valuation dispersion is wide

A capex-linked sample basket (market snapshot, 13 Mar 2026 UTC) shows meaningful dispersion:

- Lower range names: high-teens to low-20s P/E

- Mid band names: roughly 35x-60x P/E

- Upper range names: around 80x-100x P/E in select counters

Inside the same broad theme, P/B multiples also span a large range (roughly low-single-digit to high-teens in this sample).

Why this matters

When dispersion gets this wide, broad theme buying becomes blunt. You need a repeatable stock-quality framework.

The make in india stocks valuation framework (4 pillars)

Score each company across four pillars. Keep the process simple and repeatable.

1) Execution proof

Question: Is announced opportunity converting into delivered output?

What to track:

– Backlog conversion pace

– Commissioning/on-time delivery trend

– Slippage commentary versus earlier guidance

2) Margin durability

Revenue growth is not enough if margin quality is weak.

What to track:

– Gross and EBITDA margin stability

– Input-cost pass-through structure

– Mix quality (high-value vs low-margin execution)

3) Cash conversion quality

This is usually the toughest filter, and often the most useful one.

What to track:

– CFO trend versus earnings trend

– Receivable days direction

– Working-capital intensity through growth phases

For bottleneck-heavy segments, use this alongside the power T&D execution bottlenecks playbook.

4) Valuation discipline

Paying up is fine when business proof is visible. Paying up without proof is where risk rises quickly.

What to track:

– Current multiples versus own history

– Multiples versus growth durability

– Earnings revision trend versus price behavior

Theme vs fundamentals matrix

Use this 2×2 lens before adding exposure:

A) High valuation + strong delivery

- Can remain expensive for long periods

- Position sizing still matters because de-rating risk never disappears

B) High valuation + weak delivery

- Most fragile zone

- Even small misses can trigger sharp multiple compression

C) Reasonable valuation + improving delivery

- Best rerating setup if execution quality is genuinely improving

D) Low valuation + weak delivery

- Often looks cheap for a reason

- Avoid averaging down without clear improvement evidence

What must be true for current premiums to hold

For elevated capex-theme valuations to sustain, at least these conditions should stay intact:

- Backlog converts to revenue broadly in line with guidance

- Margin profile stays stable through project mix shifts

- Receivables remain controlled and cash conversion does not weaken

- Net debt and working-cap stress do not rise unexpectedly

- Earnings revisions remain constructive

- Management commentary remains specific and verifiable

If multiple conditions weaken together, valuation risk rises fast.

Common valuation mistakes in capex themes

- Treating order inflow as final proof of earnings quality

- Ignoring receivables and CFO trends during growth phases

- Using only theme-level narratives without company-level filters

- Extrapolating peak multiples to the entire basket

Practical portfolio use

A practical operating sequence:

- Start from theme context (hub view)

- Narrow to segment

- Score companies on the four pillars

- Remove names with weak cash-conversion signals

- Size exposure after valuation sanity checks, not before

This keeps decisions evidence-led instead of narrative-led.

Bottom line

The manufacturing and capex-linked India opportunity remains meaningful. But returns are decided by execution quality and cash realization, not by headline momentum.

Use one rule for make in india stocks valuation:

Pay premium multiples only where execution, margins, and cash conversion are all visible and improving.

That is how you separate durable compounding candidates from expensive stories.

FAQ

Is high valuation always a red flag in capex themes?

No. High valuation can be justified when delivery quality and cash conversion are consistently strong.

What is the best early warning metric?

Receivable trend alongside CFO quality.

Why is P/E alone not enough?

Because P/E does not capture execution slippage, margin pressure, or working-capital stress.

How often should this check be updated?

Quarterly after results, with interim checks on order conversion and receivable movement.

This article is for educational and market-tracking purposes, not investment advice.

Share this insight

Spread the Alpha

Related Articles

More ideas that align with your trading playbook.

India Power T&D Execution Bottlenecks: Investor Playbook (2026)

Quick take The india power t&d execution bottlenecks story is simple: the capex runway is large, but returns depend on execution quality,…

India Capital Goods: How to Judge Order Book Quality (2026)

Quick take Order-book size is just a starting signal. Better stock outcomes usually come from three things: conversion quality, margin quality, and…

Make in India 2.0 Playbook: How to Track India’s Manufacturing Capex Cycle as an Investor

Quick take This can become a multi-year theme, but returns will not be linear. Policy headlines are step one. Investors make money…