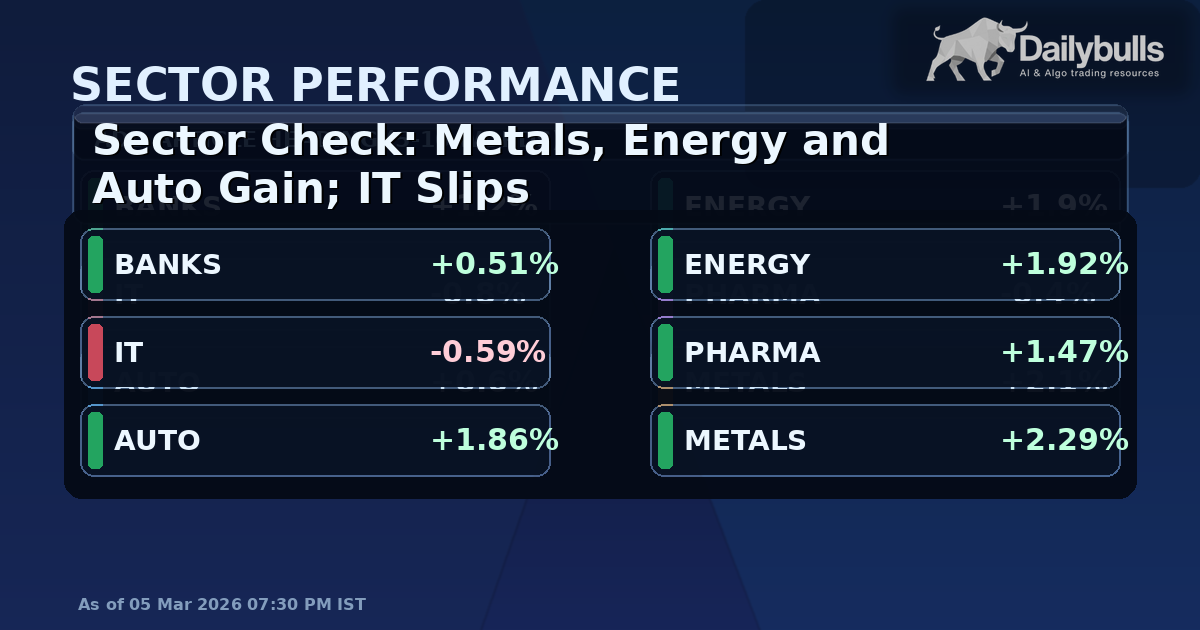

Sector Check: Metals, Energy and Auto Gain; IT Slips

End-of-day wrap: broad participation, cyclical tilt

Indian equities closed with a clear internal rotation pattern. Sector breadth was strong, with 7 sectors in green and only 1 in red. Metals led with a 2.29% gain, followed by energy at 1.92% and auto at 1.86%. IT was the only notable laggard, down 0.59%.

The gap between the strongest and weakest sector was 2.88 percentage points. This one-session dispersion shows the move was not a uniform rise across sectors.

The close reflected cyclical leadership rather than a defensive or tech-led session. With metals, energy, and auto rising together while IT trailed, market preference appeared tilted toward economically sensitive segments for the day.

What changed versus recent session tone

The most visible shift was leadership structure. Instead of a narrow rally in one pocket, the session showed cross-sector participation with a clear cyclical tilt. This adds context to index-level moves, as internal leadership changed even with moderate benchmark movement.

A second change was dispersion. The 2.88-point spread between metals and IT indicates active repricing across sector styles. This suggests selective allocation rather than uniform buying.

A third change was IT placement. With most tracked sectors positive, IT closing negative indicates internal rotation rather than broad weakness. On a session basis, this is a transition signal, not standalone confirmation of a structural break.

The current data does not establish one confirmed cause. Possible contributors include positioning, global commodity cues, domestic flows, and short-covering. Causality remains open in this dataset.

Transmission read: where signal was strongest

The strongest transmission appeared in cyclical baskets. Metals at the top, with energy and auto also firm, is consistent with stronger session-level pricing of near-term activity and earnings sensitivity.

Broad participation (7 up, 1 down) lowers the chance of a single-theme anomaly. Still, one-day participation remains an initial signal, not durability confirmation.

The key internal split is IT underperformance against positive breadth. If this split persists, the narrative can shift toward cyclical-over-defensive preference. If it closes quickly, the session may be read as a sharp but temporary adjustment.

Next-session scenarios (neutral framing)

Scenario 1: Rotation extends

If breadth stays positive and metals/energy/auto remain near the top, the leadership shift may be carrying forward.

Scenario 2: Mean reversion day

If IT stabilises and the lead-lag spread narrows materially, the print may be interpreted as a one-day overshoot.

Scenario 3: Narrow leadership risk

If cyclical sectors stay positive but overall breadth weakens, strength may become more selective and less stable.

Scenario 4: Normalisation

If both dispersion and breadth move toward neutral, rotation intensity may be cooling and the sector profile may rebalance.

Evening context notes for tomorrow framework

- Breadth confirmation: A repeat of positive breadth would strengthen the case for a signal beyond noise.

- Leadership persistence: Consecutive sessions with similar leaders carry higher informational value than one close.

- Dispersion trend: If the lead-lag gap remains elevated, allocation stays active; if it compresses, conviction may be moderating.

Overall, the end-of-day setup is coherent: strong breadth, cyclical leadership, and clear IT lag. Directional interpretation for the next session remains conditional on follow-through.

Share this insight

Spread the Alpha

Related Articles

More ideas that align with your trading playbook.

Stocks to Watch Tomorrow in India if Global Gas Risk Cools

Stocks to watch tomorrow in India if global gas risk cools If global gas-risk premium softens overnight, Indian equities may react through…

India Market Stress Playbook: Oil, Rupee, VIX, Gas and Banks

India Market Stress Playbook: Oil, Rupee, VIX, Gas and Banks This hub connects our recent India market coverage into one working framework.…

Bank Nifty Fall: Liquidity Stress or Earnings Reset?

Bank stocks led the downside in a high-volatility session. The move was sharp, but classification is important. For next-session sector confirmation, see…