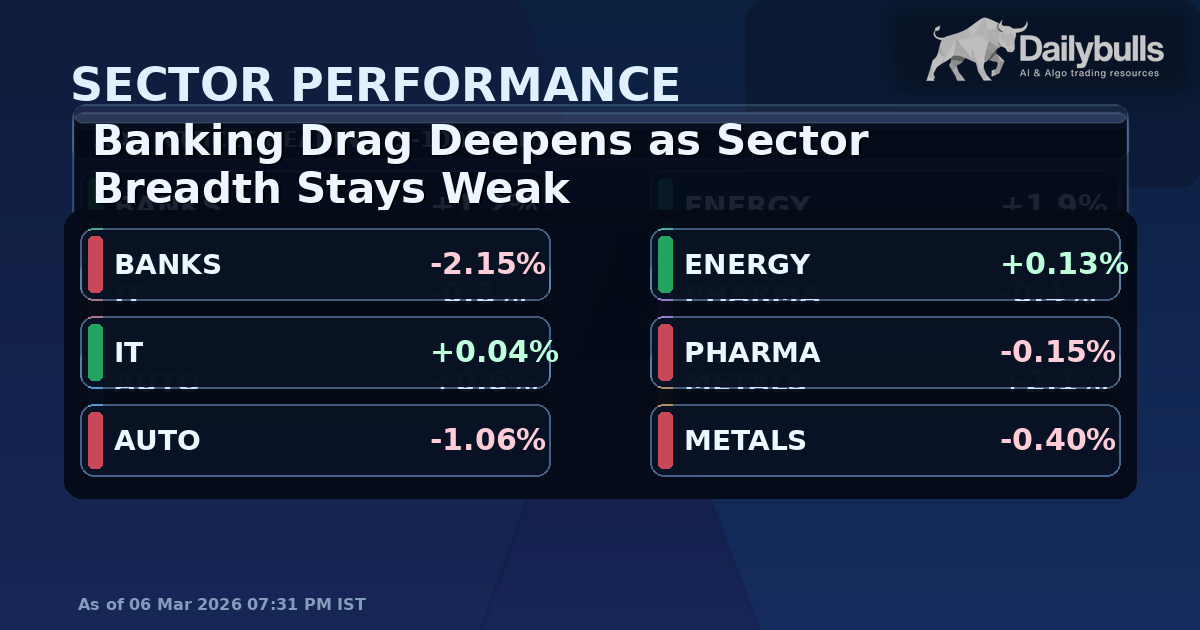

Sector Pulse: Banking Drag Deepens as Energy Holds Near Flat

Indian equities stayed under pressure in the latest session as banking weakness outweighed pockets of resilience in energy and IT. The broad signal from the tape was not a uniform selloff across every segment, but a concentrated drag from rate-sensitive and domestic-demand heavy sectors while defensives held up better.

Benchmark and sector data indicate that banks were the largest drag, with Bank Nifty down around 2.15% on the day, while energy finished modestly positive near 0.13%. Auto and realty also remained on the weak side. This created a meaningful spread between leaders and laggards, which is usually a sign of active risk re-pricing rather than passive index drift.

A key transmission channel in this move was the combined effect of higher crude and currency sensitivity. Elevated oil prices can quickly flow into inflation expectations, funding-cost assumptions, and margin expectations for segments with higher domestic credit or input sensitivity. In that backdrop, investors appeared to rotate selectively rather than exit risk in one block.

For intraday interpretation, the most important point is breadth quality. In the current setup, only a small share of tracked sectors stayed positive, while most ended negative. That weak breadth matters because it can keep index rebounds shallow unless leadership broadens beyond one or two defensive pockets.

At the same time, the divergence between sectors is useful context: when one cyclical pocket such as energy remains relatively stable while financials and rate-linked groups correct more sharply, markets are usually processing a macro shock through sector-specific balance-sheet and earnings assumptions. The session therefore reads more like a transmission move than a purely sentiment-only move.

Regulatory and policy headlines remained in focus during the day, including fresh market-facing updates in the primary market and disclosure stream. At this stage, those updates are better read as context multipliers rather than standalone direction drivers. The immediate price response still appears to be anchored mainly to macro-sensitive channels: oil, currency pressure, and risk appetite in financials.

What changes the tone from here is follow-through, not the first print. If banking weakness persists for another session while breadth stays narrow, the market may continue to trade in a selective-risk mode. If breadth improves and lagging sectors stabilise, the current move can settle into a shorter adjustment phase rather than an extended drawdown narrative.

For now, the clearest read is this: leadership is thin, sector dispersion is high, and market conviction is uneven. That combination typically keeps intraday swings elevated and pushes participants to focus on sector quality rather than only benchmark direction.

This report is informational and based on latest available market and sector snapshots; evolving developments may change the transmission path in subsequent sessions.

Share this insight

Spread the Alpha

Related Articles

More ideas that align with your trading playbook.

Stocks to Watch Tomorrow in India if Global Gas Risk Cools

Stocks to watch tomorrow in India if global gas risk cools If global gas-risk premium softens overnight, Indian equities may react through…

India Market Stress Playbook: Oil, Rupee, VIX, Gas and Banks

India Market Stress Playbook: Oil, Rupee, VIX, Gas and Banks This hub connects our recent India market coverage into one working framework.…

Bank Nifty Fall: Liquidity Stress or Earnings Reset?

Bank stocks led the downside in a high-volatility session. The move was sharp, but classification is important. For next-session sector confirmation, see…