SEBI’s Commodity Plan Just Lost Its Institutional Anchor. What It Means for MCX

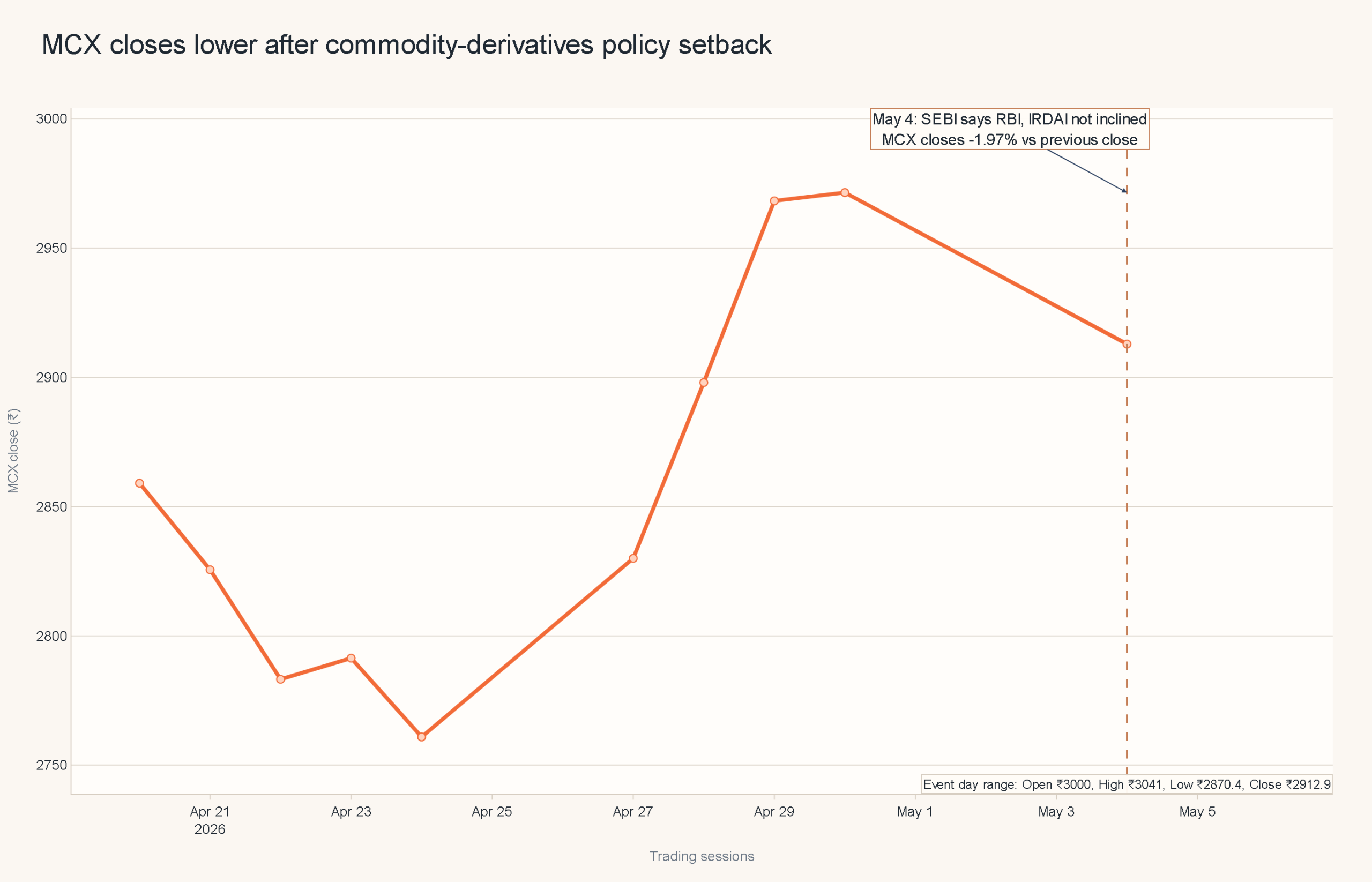

MCX did not fall because commodity markets suddenly stopped mattering. It fell because the market was forced to confront a much narrower problem: SEBI’s institutional-liquidity roadmap for commodity derivatives just got weaker.

On Monday, SEBI Chairman Tuhin Kanta Pandey said the Reserve Bank of India and the Insurance Regulatory and Development Authority of India are not inclined to allow banks and insurance companies to invest in commodity derivatives. That comment matters far beyond one policy headline. It directly undercuts the most credible institutional pathway SEBI had for deepening a market that still struggles to attract the kind of stable, long-duration participation that equity markets take for granted.

The market reaction was immediate. Shares of Multi Commodity Exchange of India fell after the comment because the readthrough was obvious. If banks and insurers remain outside the commodity-derivatives ecosystem, the cleanest case for structurally stronger market depth becomes much harder to argue.

What exactly broke on Monday

SEBI’s broader agenda was never just about adding more participants for the sake of optics. The regulator had been working with the idea that commodity derivatives needed stronger institutional participation if they were to become deeper, more resilient, and less dependent on shorter-term speculative volume.

Banks and insurers were central to that thesis. They were not just another category on a wish list. They were the most credible starting point for a more stable institutional layer because they sit on large balance sheets, manage long-duration capital, and could have added a more predictable base of participation over time.

That is why Pandey’s statement matters. It does not merely delay a reform. It weakens the foundational assumption behind the reform path itself.

Why banks and insurers mattered so much

A deeper commodity market cannot be built only on episodic retail interest and fragmented hedging demand. It needs participants that can absorb volatility, provide continuity, and help reduce the stop-start quality that often defines thinner derivatives segments.

Banks and insurers could have helped provide exactly that. Their participation would have signalled that commodity derivatives were moving closer to becoming a mainstream institutional asset class rather than a narrower trading venue. That, in turn, would have improved the long-term case for exchanges like MCX, because exchanges ultimately benefit not just from turnover but from confidence in the durability and quality of market participation.

This is the part the market understood quickly. When the two most important regulatory gatekeepers signal disinclination, the problem is no longer about timing. It becomes a question of whether the original institutional-liquidity roadmap was too dependent on participants who were never likely to be approved.

The broken assumption in SEBI’s plan

SEBI still has room to engage with other regulators and push for broader access over time. But the sequence now looks much less convincing.

The original market-deepening logic appeared to be fairly straightforward. First, bring in banks and insurers. Then expand the case for pension funds and other long-duration institutional capital. Over time, that process could have created a thicker liquidity base and a stronger hedging ecosystem.

That sequence now looks broken at the very first stage.

Pandey did not say pension funds were ruled out. But he also did not offer any indication that the pension-fund regulator had cleared a path. That leaves the most promising remaining institutional cohort in a regulatory grey zone. And once banks and insurers are no longer the first domino, the broader chain becomes much harder to build with confidence.

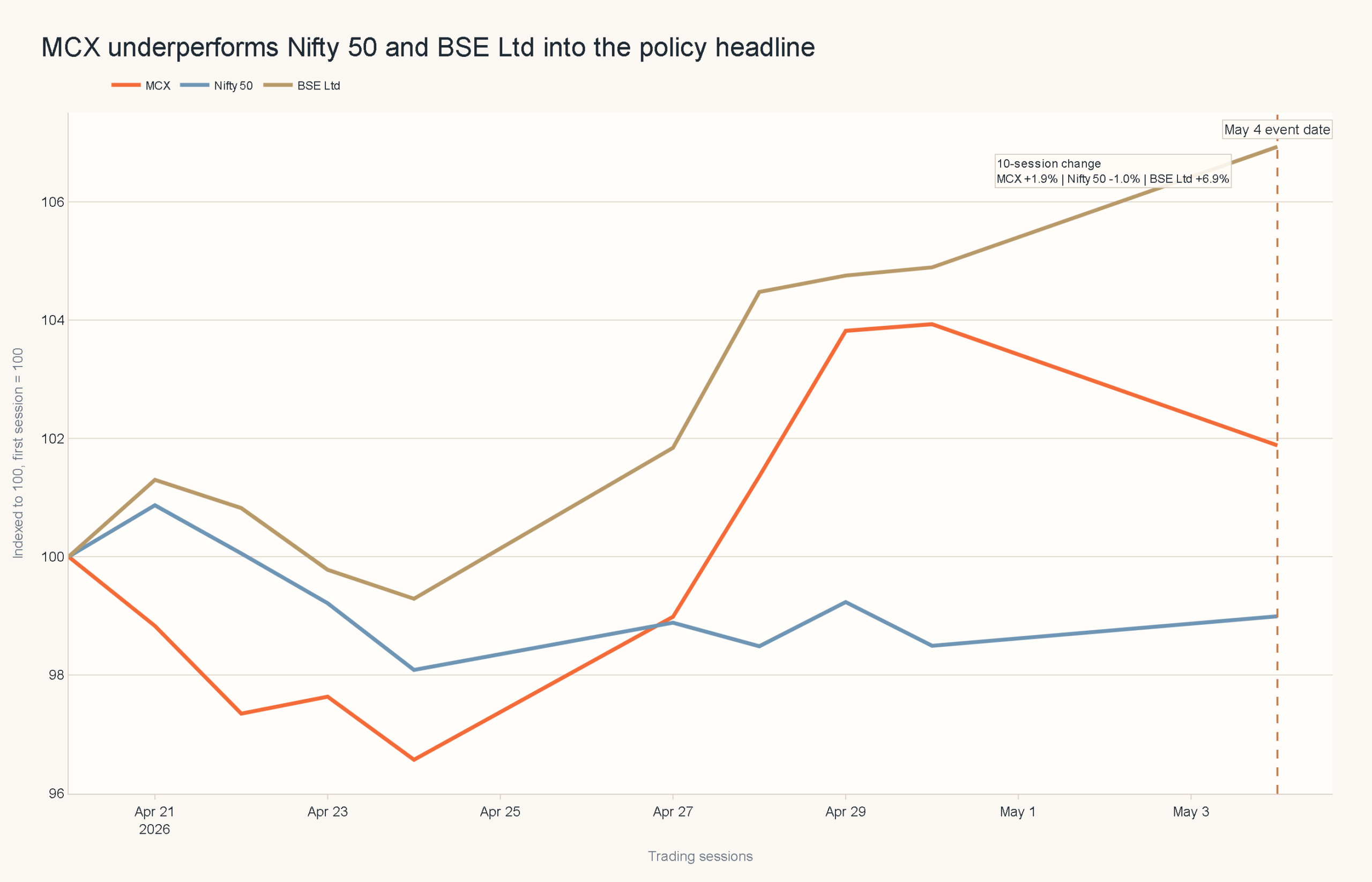

Why MCX reacted immediately

The market does not wait for a policy obituary when a valuation thesis gets weaker. It reprices as soon as the probability of the original story falls.

That is what happened to MCX.

The exchange’s long-term bull case was never just about near-term commodity price volatility or retail trading interest. It also rested on a more structural story: over time, India’s commodity markets could attract stronger institutional participation and therefore command better depth, broader participation, and more durable revenue quality.

Monday’s comment weakens that structural story. Not permanently, and not beyond repair, but enough to justify a reset in expectations.

That is why policy-led pressure on capital-market stocks can matter even before the underlying business impact fully shows up in reported numbers.

The issue is not that commodity derivatives suddenly become irrelevant without banks and insurers. They do not. The issue is that the cleanest route to a more mature institutional market now looks blocked.

The structural demand void this creates

A commodity exchange can function without banks and insurers. But it cannot easily replace what those participants were supposed to represent.

What is now visible is a structural demand void.

Without regulated balance-sheet players, the exchange remains more dependent on retail activity, tactical traders, and a narrower set of hedgers. That may be enough for day-to-day functioning, but it is weaker than the institutional-depth model SEBI appeared to be aiming for.

This matters because commodity-market quality is not only about turnover. It is also about the composition of that turnover. A market with deeper and more stable institutional participation tends to support better liquidity, smoother hedging, and stronger resilience during stress. A market without that anchor can still trade actively, but it is more vulnerable to thinner patches, sharper swings, and a more uneven depth profile.

That is why the problem is larger than MCX’s one-day move. The exchange reacted first because it is the cleanest listed proxy. But the deeper issue is that India’s commodity-market deepening story now has a visible gap where its most plausible institutional anchor was supposed to be.

Can SEBI still salvage the roadmap?

Not all paths are closed. But the substitutes are weaker.

SEBI can still push for broader participation from other investor classes. It can work on product design, retail access, liquidity incentives, and perhaps more foreign participation where regulations permit. It can continue to engage on pension-fund access, which remains unresolved rather than clearly rejected.

But none of these are a perfect substitute for what banks and insurers would have represented.

That is the real problem. The market was not assigning value only to additional volume. It was assigning value to the possibility of a more stable institutional base. Retail expansion is useful. Better products are useful. Foreign participation may help in parts. But they do not fully replicate the confidence effect that would have come from domestic regulated institutions being allowed into the market.

The tradeable takeaway

The important distinction here is between survival and structural improvement.

Commodity exchanges can survive without banks and insurers. The question is whether they can deliver the kind of structural market-depth improvement that SEBI seemed to be building toward. Monday’s signal from RBI and IRDAI makes that outcome materially harder.

That is why MCX reacted immediately, and why the move should not be dismissed as a one-day headline wobble. The market was repricing a weakened institutional-liquidity thesis.

The clean bull case for commodity exchanges has not disappeared. But it now carries a heavier regulatory discount.

For investors in exchange names, the real question now is whether SEBI can reopen the participation-expansion agenda through another regulatory route.

That is the real message. This was not just a policy setback. It was a reminder that some market-expansion plans depend less on the ambition of one regulator and more on the willingness of the other gatekeepers to open the door.

Not investment advice. Always do your own research before trading.

Share this insight

Spread the Alpha

Related Articles

More ideas that align with your trading playbook.

Reliance AGM 2026 Highlights: Jio IPO, AI and New Energy Plans Explained

Reliance Industries’ annual general meetings usually come with big announcements. The 2026 AGM was no different. But beneath the new products, ambitious…

India’s Data Center Power Trade: Which Stocks Benefit First if AI Infra Spending Accelerates?

India's AI buildout may look like a software story, but the first listed winners could emerge from transformers, cables, switchgear, backup power,…

If Brent Holds Above $120 for 2 Weeks, Which Indian Sectors Reprice First?

A one-day crude spike can be ignored. Two weeks above $120 Brent is different. At that point, Indian markets stop treating oil…

DailyBulls (Arthashilpi Ventures) is a D-U-N-S verified company.

DailyBulls (Arthashilpi Ventures) is a D-U-N-S verified company.