The Role of GST in Trading Activities: What Every Trader Should Know

Synopsis:

This blog highlights how GST affects trade in India from registering under GST to ITC benefits such as GST rates and return filing. Besides, it also describes typical challenges faced by traders like compliance issues and staying updated with the latest and changes. It presents practical tips to traders on how they can deal with GST efficiently, bring down their costs, and grow their business further.

Overview

Transforming the trade scenario in India, the Goods and Services Tax (GST) has simplified the tax structure, followed by making it more transparent and compliant-friendly. It has substituted multiple indirect taxes like VAT, CST, service tax, and so on, comprising unified systems that minimise paperwork remove cascading taxes and ensure fair pricing. The Input Tax Credit (ITC) mechanism is making traders benefit from lower tax burdens and profitability boost. GST has promoted intra-state trade through the introduction of an integrated tax between centres and states; removing entry barriers, smooth movement of goods; and finally making it easier to do business through the provision of technology-based compliance requirements such as online registration and e-invoicing. Yet GST makes competition and price similarity possible among traders, with constant governmental changes and an extravagant bookkeeping system as a prerequisite to keeping pace with compliance. Otherwise, GST revamps trade activities to a techno-savvy, fair, and comprehensively accessible business environment.

GST Registration for Traders

GST Registration is mandatory for traders who supply goods or services in India’s single tax system. Here are the eligibility criteria, process and documents required for it.

Eligibility criteria for GST registration

Traders must register for GST if they meet any of the following conditions:

Aggregate Turnover:

Service providers whose aggregate turnover is above 20 lakh in a year need to register for GST. However, this limit is 10 lakh for special category states. Similarly, entities supplying only goods need to register for GST if their turnover is above ₹40 lakh.

Inter-State Business:

All companies which supply goods interstate (from one state to another) need to register for GST regardless of their sales. Here, registration is required only for interstate service providers with turnover above ₹20 lahks, the threshold is reduced to ₹10 lahks for special category states.

E-commerce Platform:

Any person supplying goods or services through an e-commerce platform, e.g. Amazon or Flipkart needs to apply for GST registration, regardless of their turnover. Otherwise, it will be smooth sailing for all online sellers doing business through digital marketplaces.

Casual Taxable Persons:

Any person who sells goods or services occasionally or seasonally – such as through some temporary stall shop or operation – needs to register for GST without considering the income. They are thus exempted from all temporary operations for tax compliance.

Voluntary Registration:

Entities are also permitted to obtain voluntary registration under GST even when their turnover is below the prescribed limit. Hitherto, such entities were not allowed to cancel their registration within a year, but now the changes admit that voluntary registration can be cancelled at any time.

It also assures compliance and promotes business transparency, leading toward a better tax system.

The process of GST registration

To apply for GST you have to follow some steps as mentioned below:

Go to the GST Portal: One can reach the official GST portal which is gst.gov.in.

Create Log In: Register with a valid email ID, Mobile number, and PAN to create a Temporary Reference Number (TRN) for logging into the system.

Fill-up Application: Log in with TRN and fill out the application form (Form GST REG-01) along with business details.

Submit Documents: Required documents might include PAN, proof of business address, and identity verification documents.

Verification: For verification, the application would be contacted by a GST officer. Any discrepancies will be informed for correction.

E-GSTIN: After the application is approved, it can be issued with a unique E-GST identification number and registration will be completed.

Documents Required for GST Registration

- Personal Identification – PAN card for the business or owner, Aadhaar card of the proprietor, partners, or directors.

- Business Registration Proof – Certificate for company incorporation or business registration certificate.

- Address Proof – Lease agreement, electricity bill, or property tax receipt of the business premises.

- Bank Details – Cancelled cheque or bank statement.

- Photographs – Passport-sized photos of the business owner or partners.

- Digital Signature – Required for online submission of forms.

Input Tax Credit (ITC) and Its Benefits

Under the earlier indirect tax scheme, certain taxes like CST or entry tax were not creditable against purchase taxes; hence, the traders would not be able to claim any credits against these taxes. GST has simplified the entire complex process by merging all these taxes and allowing traders to avail of the Input Tax Credit (ITC) for most purchases of goods and other inputs. The import of goods has even been encompassed by the GST much-talked-about internal realised Standard Value-added tax for all purposes to offset taxes on further supplies. The credit flow of IGST on imports and receiving refunds for IGST paid on exports can use the GSTIN. Therefore, the vendor selling imports will need to possess an Import Export Code (IEC) plus the GST registration to clear customs.

The Input Tax Credit is a feature of GST which aims to remove the cascading tax effect and thus affect business cost reduction. This overturns that concept whereby a registered person can account for all GST he would have paid during purchases of goods and services against the tax liability he has on the supply of goods or services. For instance, a manufacturer buys raw materials worth Rs 10,000 and pays Rs 1,800 as GST (16%) as he bought raw materials worth Rs 10,000. ITC of Rs 1,800 can be claimed by him. If they sell goods worth Rs 15,000 and collect Rs 2,700 in GST, they can use the ITC of Rs 1,800 to reduce the amount payable, leaving only Rs 900 to be paid as GST. It provides the facility of taxation on the value added at every stage and thereby lowers the taxation burden.

Eligibility criteria for ITC

There is a negative list under Section 17(5) of the CGST Act which keeps certain transactions and businesses out of the scope of the ITC claims. These items will not bear ITC. Apart from this negative list, all the other items are eligible for claims.

Some activities that do not qualify as input tax credits are listed below:

- Motor Vehicles: Used for personal purposes (except resale, commercial purposes, and forced cab services).

- Food and Beverages: For catering, health, and similar services required by law.

- Membership Fees: Club or gym memberships.

- Insurance: Health and life insurance do not cover government mandates.

- Construction Expenses: Building immovable property.

- Lost or Destroyed Goods: Damaged or gifted items.

How to claim ITC effectively

People registered and interested in claiming ITC in GST will want to follow the below points worth mentioning to the query- how to claim ITC in GST:

- Analyse Input Tax Credit Respective to GSTR-2B: GSTR2B is an auto-generated statement reflecting returns filed by the suppliers.

- The invoice-wise ITC will match with that reflected in GSTR-2B as per the books.

- Besides, declare the output tax liability and input tax credit that is matched in the previous step while filing GSTR-3B; that is the monthly return.

- Follow up with your suppliers to clear out any possible mismatched ITC.

- Reconcile such differences & claim it in next month’s return.

- The taxpayers should remember to reverse any excess input tax credit claimed along with prescribed interest.

Claiming input tax credit would reduce the tax burden that suppliers and businesses have to bear. In addition, it also leads to a smooth and continuous flow of credits under the GST regime. Following the steps and rules to claim input tax credit makes the taxpayer eligible for all of these benefits in GST and improves profits and cash flows.

GST Rates Applicable to Trading Activities

Every trader must be aware of the applicable GST rates as applicable for different categories of goods and services traded. Here are some of the important GST rates commonly applicable to traders:

Standard Rate-18%:

It is the major rate applied to goods and services such as consumer electronics, professional services including IT, etc,

Reduced Rates-12% and 5%:

For semi-luxury goods and services artificially restricting an applicable GST of 12%. In this category certain food products like rice, wheat, and materials for construction 5% were set for essential goods like edible oils, grains, and public transportation services.

Luxury Goods:

The 28% tax is applied on luxury goods like high-end cars, air-cons, and premium household goods. Alcoholic drinks and also gambling would come under this slab.

Zero-Rated Exports:

Normally, exports are zero-rated: No GST applies when goods and services are exported outside India, meaning exporters can get a refund for taxes paid on inputs.

Exemptions:

Certain goods and services exempt from objection against GST include basic food items, in addition to healthcare services and education.

Factors Determining the Applicable GST Rate

A product or service-GST rate is usually determined considering the various types of factors which are listed for ensuring conformity with the nature of items or services, by the above factors, regional considerations and type of transaction. The important determinants are as under :

- Type of Product or Service:

GST applies according to different categories or classifications of goods or services into various tax slabs like 5%, 12%, 18%, and 28%. Generally, essential commodities, for example, food, health products and education activities, incur lower rates of GST while luxury commodities or services would include much higher rates like expensive cars and drinking alcohol. In addition, some goods and services may either have no GST or may be subject to some special rates, for example, petroleum products and electricity. - Special Category States:

States undergo categorisation in India under special category states (SCS), for example, the states in the northeast with Jammu and Kashmir. A state may have reduced GST thresholds or avail of such support from the central government in terms of finance to boost the economy. Thus, the states will have another rule regarding GST level registration requirements, special tax exemptions, or lower GST for an item related to the conditions of the regional economies, mostly for the support of small businesses. - E-commerce Transactions:

E-commerce sales, whether goods or services are always taxed subject to specific rates which may differ from those applied to an ordinary retail sale. In effect, the operators handling e-commerce shall collect GST from the sellers at the point of sale on behalf of the sellers and remit it to the government. That is the Tax Collected at Source (TCS) mechanism. Variations in the GST applicable on items sold through e-commerce depend on the type of supply made or to be made through the e-commerce platform. - Nature of Transaction (Interstate vs. Intrastate):

The location between the buyer and seller matters when determining which GST rate is applicable. Inter-state transactions imply transactions in which a buyer and seller are in different states. Such transactions necessarily come under Integrated GST, which combines both Central GST (CGST) and State GST (SGST). IGST is charged at a point of supply and divided between the central government and state government. The case for intrastate, however, is different. In this case, it means the buyer and seller are located within the same state. The tax imposed on such a type of transaction is CGST and SGST, with the two portions going to the different governments. Since revenue is shared, both state and central governments will need to share the revenue resulting from intrastate sales.

HSN Codes and their Role in GST

HSN Codes are standardized coding systems all across the world to classify goods. It significantly determines an ideal GST rate for goods and thus plays a critical role in an absolutely smooth and consistent taxation process for goods. HSN was incorporated into the Indian system in 1986 when the Central Excise and Customs Act were enacted and continues to be an important arm in the Goods and Services Tax (GST) legislation.

HSN Code Structure:

HSN codes are typically made in six digits. The first two digits refer to the chapter, the next two digits indicate the heading and the last two digits tell the subheading or product of that chapter. HSN code “0101” refers to “live horses” under the category of animal products.

Role in GST:

Goods are classified under HSN codes, and the goods classification under different HSN codes is linked with a specific GST rate. Traders must supply such an HSN code while furnishing the GST return for tax applicability. This system has been designed to standardise the classification of goods, such classification would then prove beneficial to the trader in compliance with taxation needs and requirements domestically as well as internationally.

HSN Code Requirements Based on Turnover:

- There is no compulsion for businesses below the turnover of INR 1.5 Crores to follow HSN codes for GST compliance.

- On the other hand, businesses falling between INR 1.5 Crores and INR 5 Crores must use 2-digit codes to have HSN under GST.

- For those with a turnover of more than INR 5 Crores, a business would have to have a 4-digit HSN code supposed to be accurate for classification and GST application.

- Importers and exporters: These businesses must follow 8-digit HSN codes for the proper validation through customs and tax compliance with international standards.

HSN for Services:

Similar to goods, services have been further classified into codes, known as SAC (Services Accounting Codes). The SAC codes serve the same purpose as HSN codes but are about services. These codes help to determine the GST rate applicable for various services provided by businesses.

GST Return Filing

GST Return is simply a return that captures every financial operation of an individual or business entity registered under GST of the month for which the return is prepared. Filing this GST return is compulsory for all GSTIN holders for ease of computation of net tax liability by the tax authorities.

The process of filing a GST Return involves key components:

Purchases: Copies of all the records of the purchases the taxpayer made.

Sales: The complete sales history of the taxpayer.

Output GST (on Sales): The GST that is levied to customers in the consumption phase or the GST from sales transactions.

Input Tax Credit (GST Paid on Purchases): The GST charged on goods that can be recovered as an expense in arriving at the GST chargeable on the sales.

We have developed easy-to-use, affordable GST software for GST return filling or other GST compliance needs through Vakilsearch.

Types of GST returns

Any business or individual liable to be registered under GST rules is required to file GST returns. This obligation applies only to entities with an annual aggregate turnover exceeding the set limit which may vary depending on the type of taxpayers and the classification of their activity: standard and simplified taxpayers, including composition scheme.

Of the 13 returns in the Goods and Services Tax (GST) regime, they serve various aspects of a taxpayer’s financial transaction. As much as it is crucial to highlight that not all taxpayers are going to file every type of return; it only depends on the category of the particular taxpayer as well as the specifics of GST registration.

Below is a snapshot of the 13 GST returns:

GSTR-1: Known as filed for inward supplies, that is the details for the outward supplies or in simple terms, the sale.

GSTR-3B: Commonly known as a summarised return that provides an overall picture of the business by providing details on sales made and amount spent on purchases including tax.

GSTR-4: Applicable to those under the Composition Scheme, this section gives the summarization of turnover and relative tax.

GSTR-5: Tax information on sales for non-resident taxpayers having taxable business operations in India.

GSTR-5A: For providers of Web-based information and database search and/or information delivery services, therefore.

GSTR-6: Information which Input Service Distributors use to explain the distribution of input tax credit.

GSTR-7: For legal personing, it is supposed to deduct tax at source under GST.

GSTR-8: For submission by e-commerce operators to declare activities of the e-commerce platform.

GSTR-9: A statement that provides information on all frequent submissions made periodically in a fiscal year simplified in an annual return.

GSTR-10: To the extent of operations’ it is the last payment on account resulting from the cancellation or surrender of the registration.

GSTR-11: For those with a Unique Identity Number, in an attempt to get refunds for their purchases.

CMP-08: An annual statement for Composition Scheme taxpayers about the amount of tax to be paid.

ITC-04: Manufacturer used for declaring information about goods supplied to and job worker and goods returned by the job worker.

Additionally, there are return-related statements for input tax credits:

GSTR-2A (dynamic): Provides a current view of supplies as suppliers are documenting it.

GSTR-2B (static): Offers a static view of inward supplies using the filings of the suppliers involved in a transaction.

For small taxpayers registered for the QRMP scheme, the Invoice Furnishing Facility (IFF) allows B2B sales declaration during the first two months of a quarter. However, these taxpayers are bound to pay taxes every month through the form PMT-06.

Due dates for filing GST returns

| GST Return | Type of Taxpayer | Description | Due Date |

|---|---|---|---|

| GSTR-1 | Regular Taxpayer | Details of outward supplies of taxable goods and services affected. | Monthly: 11th of the following month Quarterly: 13th of the month following the quarter |

| GSTR-2A (Auto-generated) | All Taxpayers | GSTR-2A is a dynamic, read-only return for the recipients or purchasers of goods and services | Auto-generated, utilised for reconciliation purposes |

| GSTR-3B | Regular Taxpayer | Summary return of outward supplies and input tax credit claimed, along with payment of tax by the taxpayer. | Monthly: 20th of the following month |

| GSTR-4 | Composition Scheme Dealer | Return for a taxpayer registered under the composition scheme under Section 10 of the CGST Act. | Annually: 30th of April following the end of the financial year |

| GSTR-5 | Non-Resident Foreign Taxpayer | Return to be filed by a non-resident taxable person. | 20th of the following month |

| GSTR-6 | Input Service Distributor | Return for an input service distributor to distribute the eligible input tax credit to its branches. | 13th of the following month |

| GSTR-7 | Tax Deducted at Source (TDS) | Return to be filed by registered persons deducting tax at source (TDS). | 10th of the following month |

| GSTR-8 | E-commerce Operator | Return to be filed by e-commerce operators containing details of supplies affected and the amount of tax collected at source by them. | 10th of the following month |

| GSTR-9 | Regular Taxpayer (Annual) | Annual return by a regular taxpayer. | 31st December of the following financial year |

| GSTR-9C | Regular Taxpayer (Annual) | Self-certified reconciliation statement. | Filed along with GSTR-9, by 31st December of the following financial year |

Penalty for Late Filing GST Returns

Late filing of GST returns attracts penalties and interest charges and is key to the additional cost firms have to incur while executing their operations. Here’s an overview of what happens if GST returns are delayed:

Mandatory Filing: Each person registered for GST has to file returns at fixed intervals, even when there is no transaction during the given period.

Cascading Delays: Failure to file means that you are unable to file for subsequent periods until the previous return is filed; this may pile the agency with several late returns.

Penalties for Late Filing: For instance, if there is a delay in filing GSTR-1 there are penalties on this that will be seen when filling GSTR-3B.

Interest on Outstanding Taxes: If taxes are payable and not paid up on or before the due date as and when the same is required to be paid then simple interest at the rate of eighteen per cent per annum is charged on the said amount from the day next following the due date till the actual payment is made.

Late Filing Fees: The late fee is Rs 100 per day for each CGST and SGST, subject to a maximum of Rs. 5,000.

Annual Return Penalties: Where the returns, including GSTR-9 and GSTR-9C, are filed annually, the amount of late fee payable is up to 0.25% of the turnover of the taxpayer of the relevant state or union territory, unless the government provides otherwise.

These losses in terms of money and functioning are some of the consequences that every business needs to overcome through timely GST compliance.

Challenges Faced by Traders in GST Compliance

Traders face several challenges under the Goods and Services Tax (GST) from compliance complexities to operational adjustments. Such challenges have a big impact on their daily functioning, financial processes, and, overall, business strategies.

Here are some common hurdles faced by traders:

1. Compliance with Complexities:

Understanding and keeping track of the detailed GST rules, filing norms, and timelines proves too challenging. Compliance is all about keeping records, reporting accurately the transactions as well as filing tool timely GST returns which becomes very difficult for traders, especially less resourceful or non-expert ones.

2. Technology Adoption:

Adapting to Digital Platforms for Tax Compliance: Another major area where small traders find large difficulties should be in transitioning to digital platforms, which now means all-around technological know-how to comply with the GST and create records for filing returns. Many such small businesses may find that they do not have the financial muscles to adopt technology for filing GST returns and maintaining record-keeping. Also, some may not find it easy to do so through their little knowledge of technology as well.

3. Input Tax Credit (ITC) Reconciliation:

Matching purchases with bills received from the vendor and making a proper claim under Input Tax Credit could be a little challenging. Often mismatches in Input Tax Credit reconciliation may result in non-compliance and affect cash flows requiring careful attention.

4. Increased Compliance Costs:

The cost implications of complying with the GST regime. The obligations of compliance come with an amount not limited to costs associated with accounting software, different sorts of professional services required, and training of staff. These additional costs will weigh down on the capacity of a smaller trader, hence costing money by reducing the margin on profit.

5. GST Return Filing Problems:

The filing of GST returns also involves various forms and specified periods of filing. The trader has to struggle to understand the types of returns, GSTR-1 for outward supplies, GSTR-3B for a summary on a monthly basis, and annual returns, which lead to errors or delays in filing.

6. Inter-State Transactions and IGST:

For such traders who transact across State borders, figuring out and applying the Integrated Goods and Services Tax can become complicated. Along with this, determining the correct ratio of IGST to CGST and SGST must be undertaken with due care and understanding of the tax implications.

7. Constant Fluctuations and Changes:

Continuous changes and modifications are being made to the existing GST provisions by the government. It becomes rather tough for a trader to remain updated about the latest changes and apply them at the right time in business operations, thus resulting in a high potential for non-compliance risk.

8. Input on Exempted and Non-GST Supplies:

All records maintenance challenges about taxable transactions like exempt supplies or non-GST supplies will have effectively high standards. Traders shall segregate the supplies distinct from one another and deal with them otherwise to avoid misrepresentation.

9. Transition Challenges:

Getting switched over to GST from the old tax regime may be confusing and troublesome initially. Business processes, accounting practices, and the understanding of what is meant by ‘GST’ as an activity during the transition may come as harder hurdles for traders.

10. Scrutiny and Audits:

Traders should keep accurate and fulfill the regulatory checklist which has become necessary due to the possibility of GST audits and scrutiny by tax authorities. Audits and the follow-up of discrepancies can become a time-consuming exercise and a painful one for the trader.

Steering such issues requires proactive measures including being updated on the latest regulations, investing in techno training, obtaining professional advice, and instituting a solid internal process to overcome such hurdles Consult a lawyer online can advise traders about audits, disputes, compliance strategies, and legal provisions for easy operations with reduced risks in a competitive marketplace.

Conclusion

The GST has made the trade landscape in India richer by simplifying the tax structure, giving more transparent access and building a highly efficient and competitive business environment. Creating a full-fledged environment under the Input Tax Credit (ITC), along with innovative inter-state trade processes, has knocked down the tax burdens and added simplicity to business operations. Despite all this, for the effective use of such advantages, traders must walk through new challenges GST compliance brings with it such as registration, timely filing of returns and proper classification of goods and services concerning the appropriate GST rates and HSN codes.

While adapting to constant regulatory change, audits, and possible conflicts is no less troubling, being well-informed and proactive spurs participant success. By now, adopting the new GST framework and rigorous compliance with it, traders can expect far more incredible profitability, efficiency in operations, and growth possibilities. Ultimately, all of this gives way to a more just and contemporary trading ecosystem supported by GST, where businesses can carry on activities in an increasingly globalised and technology-driven economy.

Share this insight

Spread the Alpha

Related Articles

More ideas that align with your trading playbook.

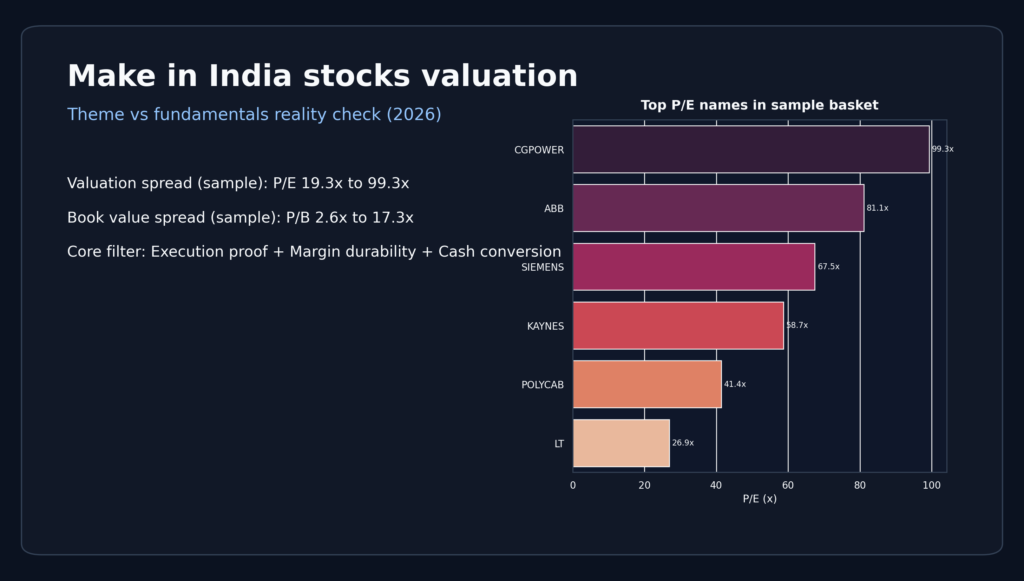

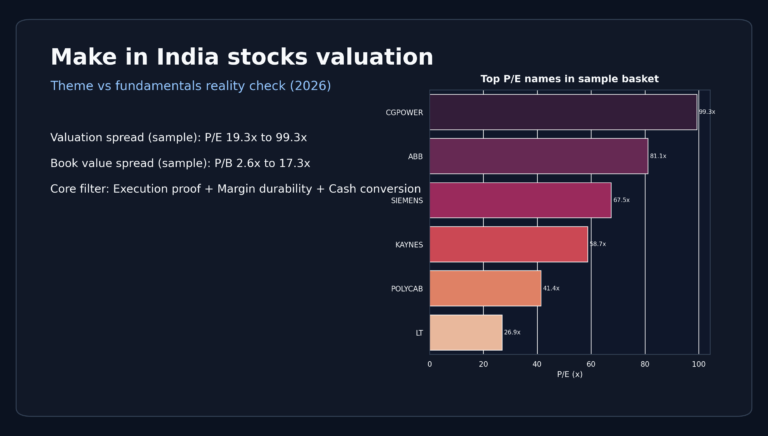

Make in India Stocks Valuation: Theme vs Fundamentals Reality Check (2026)

The Make in India manufacturing story is real. The valuation story is where things get tricky. In parts of the capex basket,…

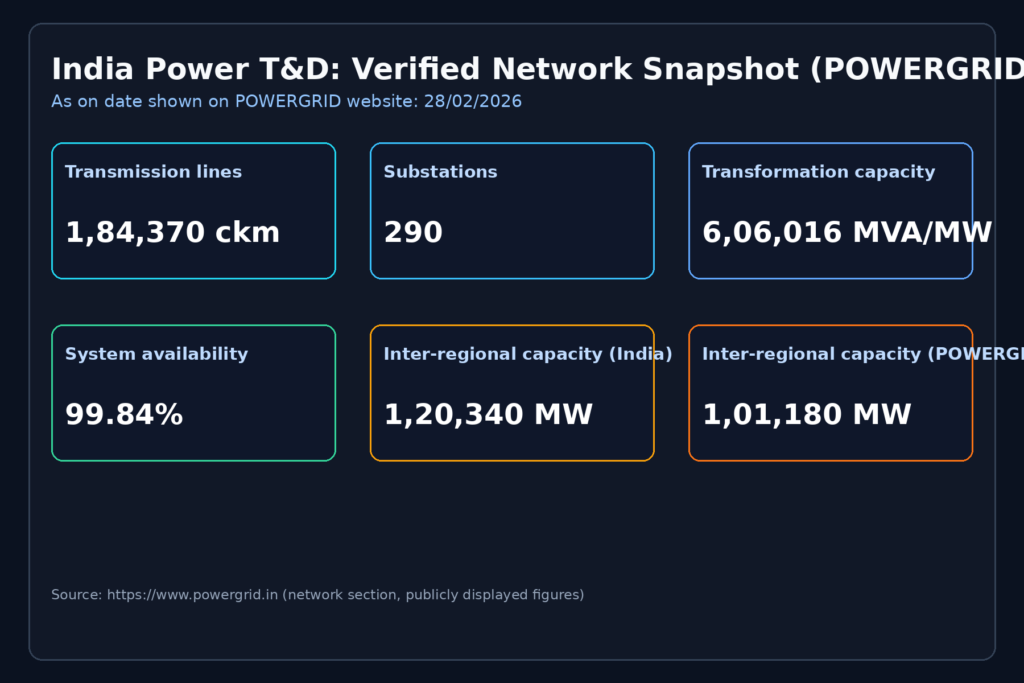

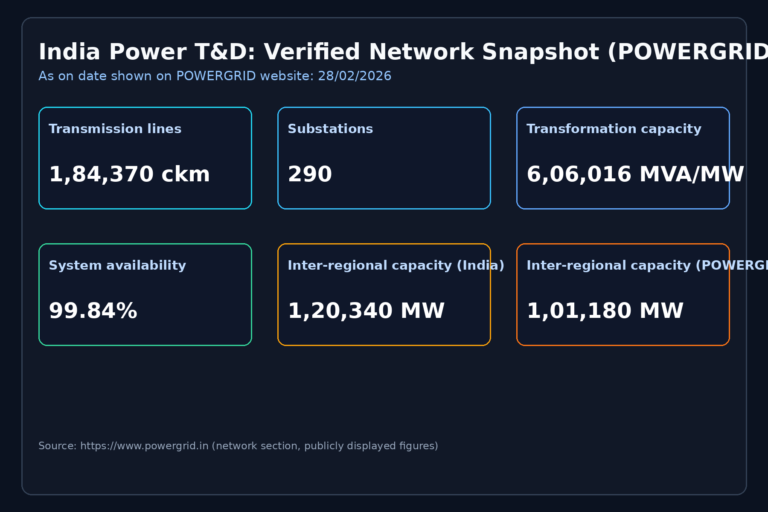

India Power T&D Execution Bottlenecks: Investor Playbook (2026)

Quick take The india power t&d execution bottlenecks story is simple: the capex runway is large, but returns depend on execution quality,…

India Capital Goods: How to Judge Order Book Quality (2026)

Quick take Order-book size is just a starting signal. Better stock outcomes usually come from three things: conversion quality, margin quality, and…