When you pledge gold for a loan, the amount you receive isn’t based on what you paid for your jewellery or what the jeweller told you it was worth. It’s based on a ratio. That ratio, called the Loan to Value ratio or LTV, is the single most important number in the entire gold loan process. Understanding how it works gives you a clear picture of what to expect before you walk into a lender’s office.

What LTV Actually Means

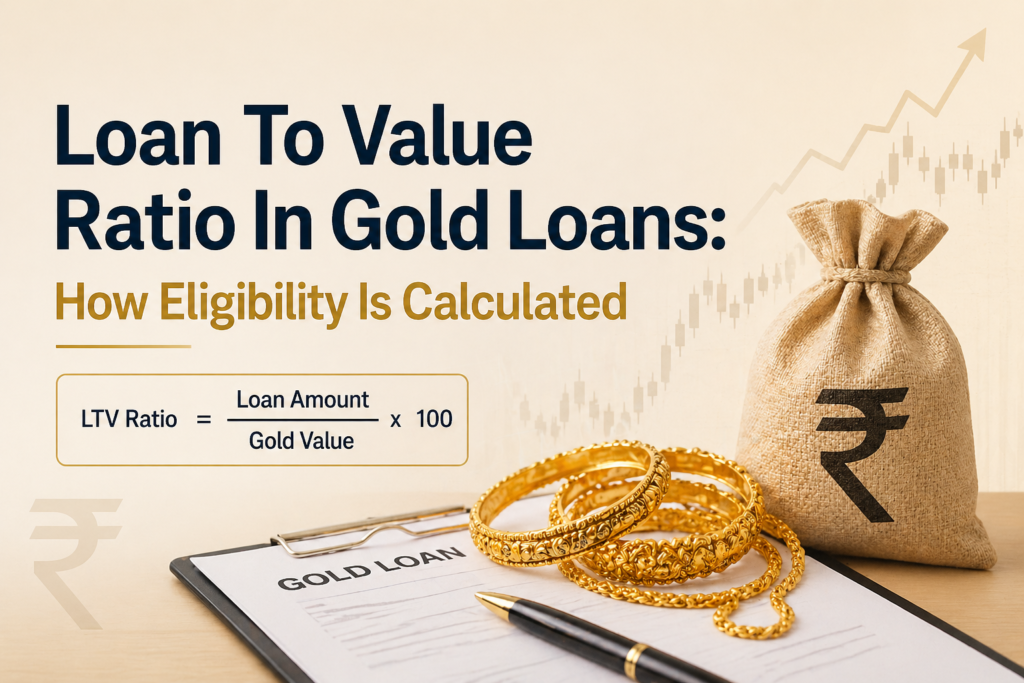

LTV is a simple fraction. The numerator is the loan amount, and the denominator is the market value of the gold you pledge. If you pledge gold worth ₹1,00,000 and receive a loan of ₹75,000, your LTV is 75%. That’s it. No complicated formula, no hidden variables.

The Reserve Bank of India caps the LTV for gold loans at 75%. This means no regulated lender, whether a bank or a non-banking financial company, can legally give you more than 75% of your gold’s current market value. Some lenders operate at lower LTV ratios, around 60% to 70%, depending on their internal risk policies. But none can cross the 75% ceiling.

This cap exists for a reason. Gold prices fluctuate. If a borrower defaults and the lender needs to auction the gold to recover the loan, there needs to be a buffer. The 25% gap between the gold’s value and the loan amount provides that buffer. When someone applies for an instant gold loan expecting to receive the full value of their gold, the LTV cap is usually the first reality check.

How Lenders Determine Gold Value

The market value of your gold isn’t based on the price you see on a commodity exchange ticker. Lenders assess the intrinsic value of the gold content only. That means the weight of pure gold in your jewellery, not the total weight of the piece including stones, enamel, or other non-gold components.

Here’s how it typically works. You bring your gold to the lender. An appraiser weighs each item, tests the purity (usually expressed in karats), and then calculates the net weight of pure gold. A 22-karat gold bangle weighing 20 grams contains approximately 18.33 grams of pure gold, since 22/24 of the total weight is actual gold. The appraiser then multiplies that net gold weight by the prevailing gold rate per gram to arrive at the gold’s value.

The prevailing rate used varies slightly between lenders. Some use the London Bullion Market Association price, others reference domestic rates published by the India Bullion and Jewellers Association. There can be minor differences between these benchmarks, which means the same piece of gold may be valued slightly differently at two different lenders on the same day.

Stones and making charges are excluded. If your necklace has embedded diamonds or precious stones, their weight is deducted before the gold value calculation. This is why heavily studded jewellery often disappoints borrowers during appraisal. The ornate piece you treasured for its craftsmanship gets reduced to its raw gold content.

Purity and Its Direct Impact on Eligibility

Gold purity matters enormously. Most lenders accept gold between 18 and 24 karats. The higher the karat, the more pure gold per gram, and therefore the higher the assessed value. A 24-karat gold coin will yield a larger loan per gram than a 20-karat gold chain.

This is where gold loan eligibility gets practical. Your eligibility isn’t really about your income, credit score, or employment status. It is almost entirely about the quantity and quality of gold you bring. A daily wage worker with 50 grams of 22-karat gold will be eligible for a larger loan than a salaried professional pledging 20 grams of 18-karat gold. The gold is the security. The gold determines the number.

That said, some lenders do perform basic KYC checks and may look at repayment capacity for larger loan amounts. But the fundamental eligibility calculation remains anchored to the gold.

Why the Actual Loan Amount Can Vary Between Lenders

Even with the same gold, two lenders may offer different amounts. One reason is the LTV each lender chooses to apply. A bank offering 65% LTV will disburse less than an NBFC offering the full 75%.

Another reason is the gold rate benchmark. If lender A uses a slightly higher gold rate reference than lender B, the assessed value will differ, and so will the loan amount.

Processing fees and interest rate structures also create practical differences. A lender offering a higher loan amount but charging a steep processing fee may leave you with less cash in hand than a lender offering a slightly lower amount with minimal fees.

What Happens When Gold Prices Fall After Disbursement

This is where LTV becomes an ongoing concern, not just an upfront calculation. If gold prices drop after you take the loan, the LTV on your loan effectively rises. Your loan amount stays the same, but the value of the pledged gold has decreased.

When the LTV breaches certain thresholds, lenders can issue margin calls. They’ll ask you to either repay part of the principal or pledge additional gold to bring the ratio back within limits. If you fail to respond, the lender has the right to liquidate your gold.

This risk is real and not hypothetical. Gold prices saw notable corrections in several periods over the past decade, triggering margin calls for thousands of borrowers. Borrowers who took loans at the maximum 75% LTV had the least room to absorb any price decline.

A Practical Approach

Before pledging gold, check the current gold rate from a reliable source. Estimate the pure gold content in your jewellery by factoring in the karat value. Apply the LTV percentage the lender advertises. That gives you a rough loan figure before you even visit the branch.

If you need a specific amount, work the math backward. Figure out how many grams of gold, at what purity, you’d need to pledge to reach that number at 75% LTV. This prevents the frustration of showing up with insufficient gold and walking away empty-handed. The calculation is straightforward, and knowing it in advance puts you in a stronger position.