How to Align Term Insurance with Your Investment Portfolio for 2025 and Beyond

Financial planning in today’s dynamic economic environment requires a holistic approach that balances wealth creation, risk mitigation, and long-term financial security. While investments like equities, mutual funds, and fixed-income instruments focus on generating returns, term insurance acts as a protective layer, ensuring financial stability for your dependents in case of unforeseen events. Aligning term insurance with your investment portfolio is crucial to achieving a well-rounded financial strategy. In this article, we will discuss how Indian investors can effectively integrate term insurance with their investment plans for 2025 and beyond.

The Role of Term Insurance in Financial Planning

Term insurance is a pure life cover that provides a high sum assured at a relatively low premium. Unlike investment-linked insurance plans, it does not offer maturity benefits. Its primary purpose is to act as a financial safety net for your family, covering liabilities and ensuring their financial independence in your absence.

In an investment portfolio, term insurance complements wealth-building instruments by addressing the “what if” scenarios, ensuring that your financial goals for your family, such as education, home ownership, and retirement planning, remain unaffected even in your absence.

Steps to Align Term Insurance with Your Investment Portfolio

1. Assess Your Financial Goals

Before aligning term insurance with your investment strategy, you need to define your short-term and long-term financial goals. Common goals for Indian investors include:

- Securing children’s higher education or marriage.

- Paying off home loans or other significant debts.

- Ensuring a comfortable retirement for your spouse.

Aligning term insurance with these goals ensures that your family’s financial needs will be met, even if unforeseen circumstances derail your investment plans.

2. Calculate the Optimal Term Insurance Coverage

The sum assured of your term insurance should align with your financial responsibilities and future goals. A general rule of thumb is to opt for coverage that is 10-15 times your annual income. However, in the Indian context, you must also consider:

- Outstanding Liabilities: Home loans, car loans, or personal loans.

- Future Expenses: Educational costs for children, family lifestyle expenses, and inflation.

- Existing Assets: Subtract investments and assets that can be liquidated in emergencies to determine the coverage gap.

For instance, if your current investments in equities and mutual funds amount to ₹50 lakhs but your family’s total financial needs are estimated at ₹2 crores, you may need term insurance coverage of ₹1.5 crores to bridge the gap.

3. Align Policy Tenure with Investment Goals

The tenure of your term insurance should coincide with your key financial milestones. If you plan to retire at 60, ensure that your term insurance covers you until then or until major liabilities, like a home loan, are paid off.

For instance:

- If you are 35 years old with a 20-year home loan, opt for a policy with at least a 25-year tenure to ensure full coverage until the liability ends.

- If your investment portfolio is designed to achieve significant growth by 2035, align the term insurance to protect your family during this critical growth phase.

4. Combine Riders for Comprehensive Coverage

While the base term insurance plan provides life coverage, riders can enhance its scope by addressing specific risks. Common riders in the Indian market include:

- Total and Permanent Disability Rider: Considering a policyholder is left disabled following an accident or a listed ailment, the insurer offers a certain sum to compensate for the compromised source of income. The disbursement of this amount can be either monthly or as a lump sum.

- Accidental Death Benefit: Increases the sum assured in case of accidental death.

- Waiver of Premium: Waives future premiums if you become disabled or critically ill.

Adding these riders reduces the need to withdraw from your investment portfolio in emergencies, allowing your wealth to grow uninterrupted.

5. Balance Premium Costs with Investment Allocations

One of the key advantages of term insurance is its affordability. For instance, a ₹1 crore term plan for a 30-year-old non-smoker could cost as little as ₹8,000 annually. This low premium ensures you can allocate a significant portion of your income to high-growth investments like equities and mutual funds.

When aligning your budget, prioritise term insurance to protect your portfolio and family while ensuring enough funds remain for wealth-building instruments.

6. Reassess Your Coverage Regularly

As your income, responsibilities, and financial goals evolve, your term insurance coverage should also be revisited. For example:

- A salary hike or a new family member (childbirth) may necessitate higher coverage.

- Significant portfolio growth might reduce the required coverage.

In the Indian context, regularly revisiting your financial plan ensures that your term insurance and investments remain aligned with your current and future needs.

Why Term Insurance Matters for Indian Investors

Inflation-Proofing Your Family’s Future

With India’s inflation rate averaging 6-7% annually, the real value of your investment returns may erode over time. Term insurance provides a fixed sum assured that safeguards your family against the unpredictability of inflation.

Tax Benefits Under Section 80C and 10(10D)

Premiums paid for term insurance qualify for deductions under Section 80C of the Income Tax Act, up to ₹1.5 lakhs annually. Additionally, the death benefit is tax-exempt under Section 10(10D), ensuring your family receives the full payout.

Affordable Protection Amid Rising Healthcare Costs

As healthcare expenses in India continue to soar, term insurance with riders like critical illness cover ensures that your family’s financial stability is not compromised by medical emergencies, allowing your investments to remain untouched.

Looking Ahead: Aligning for 2025 and Beyond

The financial landscape in India is evolving, with growing awareness about wealth management and protection. For 2025 and beyond, Indian investors must integrate term insurance as a cornerstone of their financial plan, ensuring it complements their investment portfolio.

Key trends to watch include:

- Increasing Digital Access: Term insurance policies can now be easily purchased and managed online, ensuring transparency and convenience.

- Customised Plans: Insurers are offering flexible plans tailored to individual needs, making alignment with investment goals more seamless.

By proactively aligning term insurance with your investment strategy, you can achieve financial security, peace of mind, and sustained wealth creation for your loved ones.

Conclusion

Term insurance is not just a safety net; it is an essential component of a robust financial plan. By understanding your financial goals, calculating the right coverage, and balancing it with your investment allocations, you can ensure your portfolio is well-protected against uncertainties. As you plan for 2025 and beyond, let term insurance be the anchor that secures your family’s future while your investments propel you toward your dreams.

Share this insight

Spread the Alpha

Related Articles

More ideas that align with your trading playbook.

India’s Crude Sensitivity Ladder: 10 Stocks to Watch if Brent Holds Above $120

If Brent holds above $120, Indian equities are unlikely to react in one wave. This crude sensitivity ladder ranks 10 stocks to…

Personal Finance Risk Checklist for Indian Investors: Before You Increase Equity Exposure

The first risk in equity investing is not volatility. It is interruption. A strong portfolio needs time, cash-flow stability, and a household…

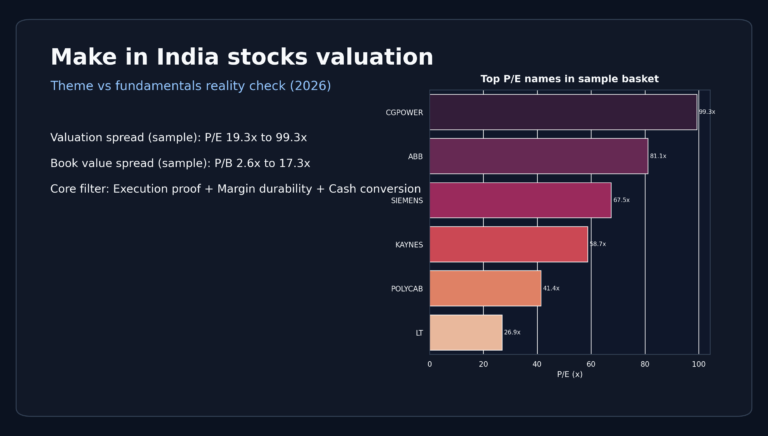

Make in India Stocks Valuation: Theme vs Fundamentals Reality Check (2026)

The Make in India manufacturing story is real. The valuation story is where things get tricky. In parts of the capex basket,…

DailyBulls (Arthashilpi Ventures) is a D-U-N-S verified company.

DailyBulls (Arthashilpi Ventures) is a D-U-N-S verified company.