Why Indian Chemical sector in declining and what to expect for future?

Despite a strong position in global markets, the Indian Chemical sector has shown timid growth since the year 2022. The industry was a global outperformer in demand growth and was a wealth creator for the shareholders for almost a decade. However, in the last few years, Chemical stocks have underperformed. The profitability and margins of Indian companies took a hit, the reason for which we will study below.

Facts about the Indian Chemical Sector

- Contributes around 7% to GDP

- Third largest producer in Asia

- Top 10 Exporter in the world

- Sector to add additional $80 million in market cap by 2030

Chemical companies past performance

For a decade, the Indian chemical industry outperformed its global counterparts with strong total shareholder returns (TSR) growing at an annual rate of 20% between 2014 and 2023, compared to the global average of 6%¹

Why is the Indian Chemical sector underperforming?

For a decade, the Indian chemical industry outperformed its global counterparts with strong total shareholder returns (TSR) growing at an annual rate of 20% between 2014 and 2023, compared to the global average of 6%¹

High input cost

Feedstocks which act as a key material for chemical manufacturing processes can greatly affect the production costs. In the chemical Industry, natural gas is one such feedstock, price for which has spiked in the last few years. In Europe, natural gas prices increased by 420% compared to 2010-2020 averages, while Asian and North American markets saw increases of 105% and 50% respectively ². Further, the high cost of materials like Alcohol and Caustic Soda, which are required in several processes also were hiked. This has put pressure on chemical companies’ production costs which hampered chemical companies margins.

Slow global demand

For Indian players, the European market is a big opportunity. However, weak economic conditions in the EU markets have trimmed the demand for chemicals. Also, after the COVID-19 crisis, a demand and supply mismatch led to slow growth. Let us understand why this mismatch happens.

Destocking

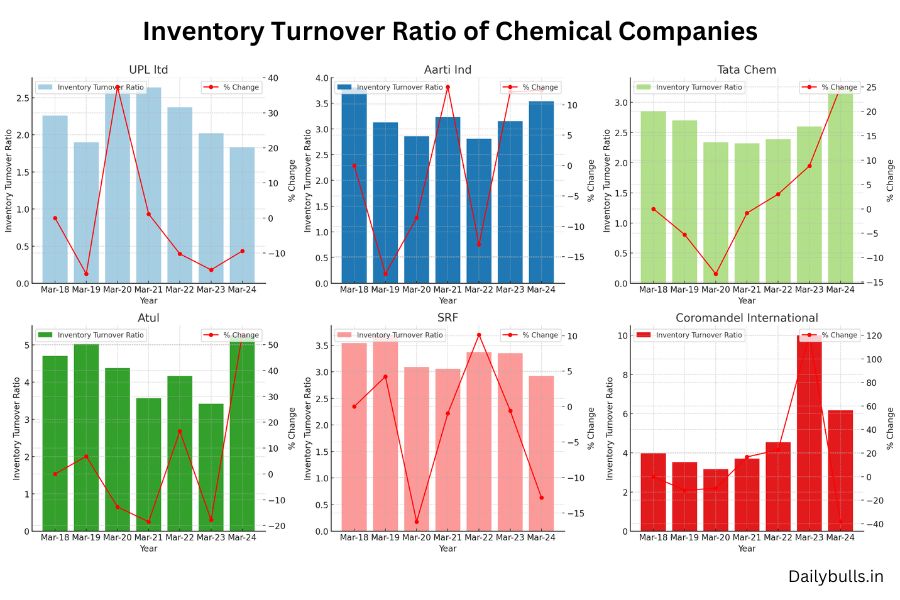

You see, during the pandemic, when the supply chain was disrupted, chemical buying companies (we will refer to them as Buyers) were concerned about the availability of raw materials. This led to overstocking in the distribution channel. However, as demand slowed in 2022-23 due to factors like inflation and economic uncertainty, chemical companies and their distributors were left holding excess inventory. This prompted buyers to actively reduce stock levels, also known as destocking. The below image shows the inventory turnover ratio of chemical manufacturers. To give an overall view, I have included data from 6 companies from different industries within the Chemical sector.

Analysis of Inventory Turnover

Inventory Turnover Ratio

A high inventory turnover ratio indicates that a company is selling its inventory quickly and efficiently, with minimal holding costs. This metric is a key indicator of operational efficiency and effective inventory management.

The inventory turnover data by UPL Ltd, Aarti Industries, Tata Chemicals, Atul, SRF, and Coromandel International is shown from 2018 and 2024. The data depicts the relative efficiencies of these companies in managing their inventories. Inventory turnover by UPL Ltd has been fluctuating upwards and peaked around 2022 and then slowly falling since then.

Aarti Industries and Tata Chemicals were moderate in stability with annual fluctuations. There is also a general upward trend in Atul industries.SRF fluctuated very slightly, but it was adhering to a constant rate of turnover. The graph for Coromandel International shows huge fluctuations with a huge peak at the end of 2023 followed by drops.

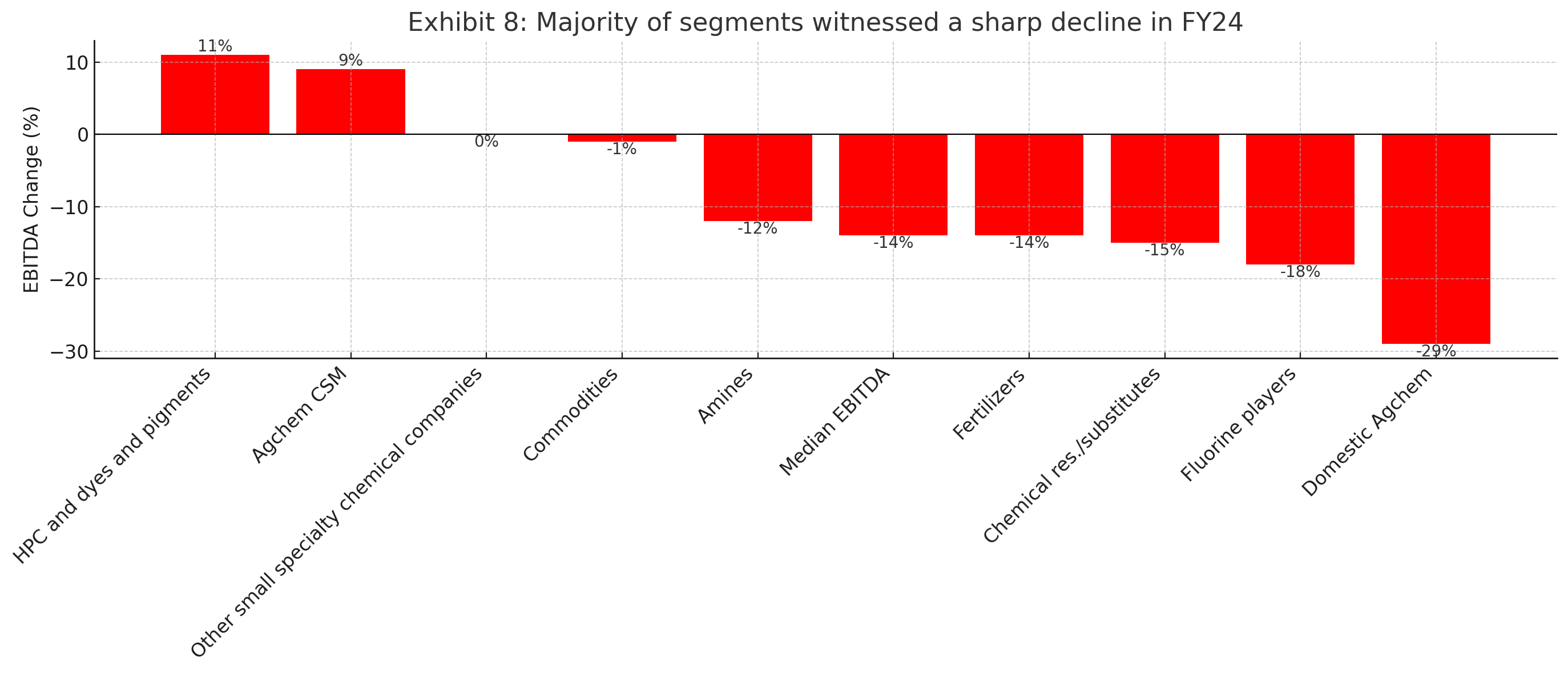

Not all industries declined

While the overall sector showcased a weak performance, some industries were relatively better. The chart below shows the EBITDA changes across various chemical industry segments in FY24, indicating a predominantly downward trend. Agrochemicals and Specialty chemicals were the only industries with positive EBITDA change in FY24.

HPC dyes and pigments and Agchem CSM are the exceptions, recording increases of 11% and 9%, respectively, suggesting robust market demand or effective cost control.

Other small speciality chemical companies and Commodities show minimal changes, with EBITDA essentially flat or slightly down.

Most other segments like Amines, Fertilizers, Chemical res./substitutes, Fluorine players, and Domestic Agchem experienced declines ranging from 12% to 29%, hinting at issues such as rising costs or reduced demand.

What to expect in Future?

The chemical sector’s outlook is showing signs of improvement. Several indicators, including PMI, new orders, and Brazilian chemical imports, hint at modest volume enhancements in the near term. In fact, UBS projects a 5-10% volume surge for Indian chemical companies. This growth is likely to be driven by economic recovery in global markets and robust domestic demand within India, both of which are expected to fuel chemical manufacturing and investments in the short term.

Talking about recovery from destocking, it is estimated that it may take the chemical industry up to 300 days to reset inventory to sustainable levels³. During this period, chemical company sales and profits are likely to remain under pressure which we are observing in current time. Below is a statement from Rohan Gupta from his interview with The Economic Times:

“Some of the companies have already started witnessing recovery from Q3. Many of them will post recovery and QoQ growth from Q4. So the sector earnings have bottomed out, that is for sure… We are still seeing the growth opportunity for the Indian chemical industry as very, very bright… the specialty chemical sector, in my view, is likely to do well over the next one year.”

China+1 and Government policies to help the sector

The fact that the structural growth drivers for the chemical sector remain unchangeable. Factors such as the China+1 strategy, Europe+1 strategy, import substitution, and the ‘Atmanirbhar Bharat‘ initiative are sure to drive growth once near-term headwinds subside. Additionally, rising domestic consumption, shifting consumer preferences towards eco-friendly products, and evolving supply chains are expected to bolster long-term growth in the sector.

The government’s role in supporting the chemical industry cannot be overlooked. Favorable policies, including 100% FDI under the automatic route and PLI schemes, are likely to attract investments and boost growth. The Petroleum, Chemicals and Petrochemicals Investment Regions (PCPIRs) are projected to draw investments worth $420 billion, underscoring the sector’s robust potential.

While the chemical sector has faced challenges in recent years, the future appears promising. With improving demand, potential margin expansion, and supportive government policies, the sector seems well-positioned for a rebound and sustained growth in the coming years.

About the author

Dailybulls Research

Senior Researcher and Editor

Dailybulls Research Team consists of experienced market analyst from multiple domains like equity, futures and options, forex and commodities. The team is focused on providing data backed research, powered by Ai and machine learning algorithms.

Share this insight

Spread the Alpha

If this analysis helped you, pass it along to your trading desk or community.

Related Articles

More ideas that align with your trading playbook.

Why Indian IT Stocks Are Really Falling: Beyond the AI Fear Story

The Indian IT sector is going through a sharp correction. While news headlines blame “AI fears,” a deeper look at the data…

Best Sugar Ethanol Stocks by production capacity

The ambitious goal of the Modi Government to transform the sugarcane belt in India as the energy belt, received a positive response…

Very interesting points you have mentioned, thanks for posting.